Finance (No. 2) Act 2013

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Number 41 of 2013 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

FINANCE (NO. 2) ACT 2013 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

CONTENTS | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Income Tax, Corporation Tax and Capital Gains Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Interpretation | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Section | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Income Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

2. Amendment of section 226 of Principal Act (certain employment grants and recruitment subsidies) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

8. Amendment of section 470 of Principal Act (relief for insurance against expense of illness) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

9. Amendment of section 469 of Principal Act (relief for health expenses) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

10. Exemption in respect of annual allowance for reserve members of the Garda Síochána | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

16. Limitation on amount of certain reliefs used by certain high income individuals | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

19. Amendment of Schedule 12 to Principal Act (employee share ownership trusts) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Income Tax, Corporation Tax and Capital Gains Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

21. Amendment of section 766 of Principal Act (tax credit for research and development expenditure) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

22. Amendment of section 246 of Principal Act (interest payments by companies and to non-residents) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

23. Amendment of Part 8 of Principal Act (annual payments, charges and interest) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

24. Amendment of section 481 of Principal Act (relief for investment in films) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

26. Amendment of section 530F of Principal Act (obligation on principals to deduct tax) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Corporation Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

32. Amendment of section 77 of Principal Act (miscellaneous special rules for computation of income) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

38. Acceleration of wear and tear allowances for certain energy-efficient equipment | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

39. Amendment of section 23A of Principal Act (company residence) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Capital Gains Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

41. Amendment of section 29 of Principal Act (persons chargeable) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

42. Amendment of section 552 of Principal Act (acquisition, enhancement and disposal costs) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

43. Amendment of section 598 of Principal Act (disposals of business or farm on “retirement”) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

44. Amendment of section 604A of Principal Act (relief for certain disposals of land or buildings) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Excise | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

46. Amendment of Chapter 1 of Part 2 of Finance Act 1999 (mineral oil tax) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

48. Amendment of Chapter 3 of Part 2 of Finance Act 2001 (offences, penalties and proceedings) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

49. Amendment of Chapter 4 of Part 2 of Finance Act 2001 (powers of officers) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

50. Amendment of Chapter 5 of Part 2 of Finance Act 2001 (miscellaneous) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

51. Amendment of Chapter 3 of Part 3 of Finance Act 2010 (solid fuel carbon tax) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

56. Amendment of section 139 of Finance Act 1992 (offences and penalties) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Value-Added Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

59. Amendment of section 59 of Principal Act (deduction for tax borne or paid) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

60. Adjustment of tax deductible in relation to unpaid consideration | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

62. Amendment of section 64 of Principal Act (capital goods scheme) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

63. Amendment of section 80 of Principal Act (tax due on moneys received basis) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

65. Notice of requirement to furnish certain information, etc. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Stamp Duties | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

71. Amendment of section 125B of Principal Act (levy on pension schemes) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Miscellaneous | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

76. Amendment of section 887 of Principal Act (use of electronic data processing) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

81. Amendment of section 851A of Principal Act (confidentiality of taxpayer information) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Miscellaneous Technical Amendments in relation to Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Acts Referred to | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Air Pollution Act 1987 (No. 6) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Building Societies Act 1989 (No. 17) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Capital Gains Tax Acts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Central Bank Act 1971 (No. 24) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Civil Partnership and Certain Rights and Obligations of Cohabitants Act 2010 (No. 24) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Companies Act 1963 (No. 33) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Corporation Tax Acts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Criminal Assets Bureau Act 1996 (No. 31) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Criminal Procedure Act 1967 (No. 12) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Customs Acts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Customs Consolidation Act 1876 (39 & 40 Vict., c. 36) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance (No. 2) Act 2008 (No. 25) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 1950 (No. 18) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 1992 (No. 9) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 1999 (No. 2) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 2001 (No. 7) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 2002 (No. 5) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 2003 (No. 3) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 2005 (No. 5) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 2010 (No. 5) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 2011 (No. 6) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Finance Act 2013 (No. 8) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Guardianship of Infants Act 1964 (No. 7) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Health Insurance Act 1994 (No. 16) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Income Tax Acts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Inland Revenue Regulation Act 1890 (53 & 54 Vict., c. 21) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Pensions Act 1990 (No. 25) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Planning and Development Act 2000 (No. 30) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Social Welfare Acts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Stamp Duties Consolidation Act 1999 (No. 31) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Succession Duty Act 1853 (16 & 17 Vict., c. 107) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Tax Acts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Taxes Consolidation Act 1997 (No. 39) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Value-Added Tax Acts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Number 41 of2013 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

FINANCE (NO. 2) ACT 2013 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

An Act to provide for the imposition, repeal, remission, alteration and regulation of taxation, of stamp duties and of duties relating to excise and otherwise to make further provision in connection with finance including the regulation of customs. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

[18th December, 2013] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Be it enacted by the Oireachtas as follows: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

PART 1 Income Tax, Corporation Tax and Capital Gains Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 1 Interpretation | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Interpretation (Part 1) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

1. In this Part “Principal Act” means the Taxes Consolidation Act 1997 . | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Chapter 2 Income Tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Amendment of section 226 of Principal Act (certain employment grants and recruitment subsidies) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

2. Section 226 of the Principal Act is amended in subsection (1)— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in paragraph (i) by deleting “or”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in paragraph (j) by substituting “applies, or” for “applies.”, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) by inserting the following after paragraph (j): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(k) as respects payments made to employers on or after 1 July 2013, JobsPlus, being a scheme administered by the Department of Social Protection.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Amendment of section 253 of Principal Act (relief to individuals on loans applied in acquiring interest in partnerships) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

3. Section 253 of the Principal Act is amended by inserting the following after subsection (7): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(8) Notwithstanding subsection (7), the deduction authorised by that subsection shall not exceed— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) as respects the year of assessment 2014, 75 per cent of the deduction that would but for this subsection be authorised by that subsection, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) as respects the year of assessment 2015, 50 per cent of the deduction that would but for this subsection be authorised by that subsection, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) as respects the year of assessment 2016, 25 per cent of the deduction that would but for this subsection be authorised by that subsection, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(d) as respects the year of assessment 2017 and each subsequent year of assessment, zero per cent of the deduction that would but for this subsection be authorised by that subsection. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(9) This section shall not apply to a loan made after 15 October 2013. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(10) Subsections (8) and (9) shall not apply to a loan referred to in subsection (1) where the partnership is a farming partnership within the meaning of section 598A. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(11) Subsection (9) shall not apply to a loan made after 15 October 2013 which is applied in paying off another loan to an individual used to defray money applied under paragraph (a), (b) or (c) of subsection (1), provided— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) the loan does not exceed the balance outstanding on the loan being paid off, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) the term of the loan does not exceed the balance of the term of the loan being paid off.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Cesser of top slicing relief | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

4. (1) The Principal Act is amended in Schedule 3— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in Part 2 by substituting “on or after the date of the passing of the Finance Act 2013 ” for “on or after the date of the passing of this Act” in paragraph 9A (inserted by section 14(1)(e) of the Finance Act 2013 ), and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in Part 3 by inserting the following paragraph after paragraph 13: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

14. Notwithstanding section 201, paragraph 10 shall cease to apply to any payment which is made on or after 1 January 2014 and which is chargeable to income tax under section 123.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(2) Subsection (1)(a) shall have effect as if it had come into operation on or after 27 March 2013. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Home renovation incentive | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

5. The Principal Act is amended— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in Part 15— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) by repealing section 477A, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) by inserting the following section before section 478: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“Home renovation incentive | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

477B. (1) In this section— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘contractor’ means a person engaged by an individual to carry out qualifying work, and who is an accountable person under section 5 of the Value-Added Tax Consolidation Act 2010 and has been assigned a registration number under section 65 of that Act; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘PPS number’, in relation to an individual, means the individual’s personal public service number within the meaning of section 262 of the Social Welfare Consolidation Act 2005 ; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘qualifying contractor’ means a contractor who— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) complies with the obligations referred to in section 530G or 530H, as the case may be, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in the case of a contractor who is not a subcontractor to whom Chapter 2 of Part 18 applies, complies with the obligations referred to in paragraph (a), other than the obligations referred to in paragraphs (a) and (b) of subsection (1) of section 530G or 530H, as the case may be; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘qualifying expenditure’, in relation to an individual, means expenditure incurred by the individual on qualifying work carried out by a qualifying contractor on a qualifying residence; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘qualifying residence’, in relation to an individual, means a residential premises situate in the State— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) which is owned by the individual and which is occupied by the individual as his or her only or main residence, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) which has previously been occupied as a residence and has been acquired by the individual for the purposes of occupation by the individual as his or her only or main residence on completion of the qualifying work and which is so occupied upon completion; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘qualifying work’ means any work of repair, renovation or improvement to which the rate of tax specified in section 46 (1)(c) of the Value-Added Tax Consolidation Act 2010 applies, and which is carried out on a qualifying residence; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘residential premises’ means— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) a building or part of a building used, or suitable for use, as a dwelling, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) land which the occupier of a building or part of a building used as a dwelling has for the occupier’s own occupation and enjoyment with that building or that part of a building as its garden or grounds of an ornamental nature; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘specified amount’, in relation to a payment in respect of qualifying expenditure, means 13.5 per cent of the amount of the payment on which value-added tax is charged, subject to a maximum amount of €4,050, provided that, where more than one payment is made in respect of qualifying expenditure, the aggregate of the specified amounts in respect of those payments shall not exceed €4,050; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘tax reference number’, means in the case of an individual, the individual’s PPS number or in the case of a company, the reference number stated on any return of income form or notice of assessment issued to that company by the Revenue Commissioners; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘unique reference number’ has the meaning given to it by subsection (4)(b); | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘VAT registration number’, in relation to a person, means the registration number assigned to the person under section 65 of the Value-Added Tax Consolidation Act 2010 . | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(2) (a) This section applies to qualifying expenditure incurred on qualifying work carried out during the period from 25 October 2013 to 31 December 2015. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) Where payments in respect of qualifying work are made during the period from 25 October 2013 to 31 December 2013, those payments shall be deemed to have been made in the year of assessment 2014. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) Notwithstanding paragraph (a), where qualifying work, for which permission is required under the Planning and Development Act 2000 , is carried out during the period from 1 January 2016 to 31 March 2016, then provided such permission is granted on or before 31 December 2015, that work shall be deemed to be carried out in the year of assessment 2015. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(3) (a) Subject to the provisions of this section, where an individual (in this section referred to as ‘the claimant’), on making a claim in that behalf, proves that in a year of assessment he or she has made a payment or payments to a qualifying contractor in respect of qualifying expenditure to which this section applies, the income tax to be charged on the claimant, other than in accordance with section 16(2), shall be reduced— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) in the case of the first subsequent year of assessment, by an amount which is the lesser of— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(I) 50 per cent of the specified amount of the payment or payments, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(II) the amount which reduces the income tax of that year of assessment to nil, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) in the case of the next subsequent year of assessment, by an amount which is the lesser of— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(I) that part of the specified amount not used in the year of assessment referred to in subparagraph (i), and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(II) the amount which reduces the income tax of that year of assessment to nil. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) Insofar as any part of the specified amount cannot be used under paragraph (a) (in this paragraph referred to as ‘excess relief’) due to the insufficiency of income tax charged on the claimant in the two years of assessment following the year of assessment in which the payment or payments referred to in paragraph (a) were made, the income tax for the year of assessment following those two years of assessment and so on for each succeeding year of assessment shall be reduced by the excess relief until the full amount of the excess relief has been used, provided that the amount of the excess relief used in any year of assessment shall not be greater than the amount which reduces the income tax charged on the claimant in that year of assessment to nil. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) The maximum amount of relief available under this section in respect of a qualifying residence shall not exceed €4,050. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(d) No claim shall be made under this section unless the payment, or where there is more than one payment the aggregate of those payments, in respect of qualifying expenditure made to a qualifying contractor or qualifying contractors is equal to or greater than €5,000. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(e) Where an individual engages a contractor to carry out qualifying work, it shall be the responsibility of that individual to be satisfied that the contractor is a qualifying contractor. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(4) (a) Subject to paragraph (c), a contractor shall, before commencing qualifying work under this section, provide to the Revenue Commissioners— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) the contractor’s name, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) the contractor’s tax reference number and VAT registration number, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iii) the unique identification number assigned in accordance with section 27 of the Finance (Local Property Tax) Act 2012 to the property on which the qualifying work is to be carried out, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iv) the name of the claimant, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(v) the address of the property at which the work will be carried out, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(vi) a description of the work to be carried out, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(vii) the estimated cost of the work to be carried out, separately identifying the amount of value-added tax, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(viii) the estimated duration of the work, including the estimated start date and estimated end date. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) On receipt of the information referred to in paragraph (a), the Revenue Commissioners shall— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) notify the contractor, as the case may be, that— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(I) the contractor is a qualifying contractor for the purposes of this section and such notification shall contain a number for the work (in this section referred to as the ‘unique reference number’), or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(II) that the contractor is not a qualifying contractor for the purposes of this section, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) where the contractor is a qualifying contractor, notify the individual concerned accordingly and the notification shall stipulate the unique reference number for the work. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) Where a qualifying contractor has commenced qualifying work on or after 25 October 2013 but before the electronic systems referred to in subsection (10) are made available by the Revenue Commissioners, the contractor shall provide to the Revenue Commissioners the information specified in paragraph (a) within 28 days of such electronic systems being made available. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(5) (a) Upon receipt of payment from the individual concerned in respect of qualifying work, but not later than 10 working days following receipt of such payment, the contractor shall— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) provide to the Revenue Commissioners the following information: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(I) the contractor’s name; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(II) the contractor’s tax registration number and VAT registration number; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(III) the unique reference number for the work; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(IV) details of the amount of the payment, separately identifying the amount of value-added tax; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(V) the name of the individual from whom the payment was received; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(VI) the date of the payment, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) provide to the individual a statement showing the amount of the payment separately identifying the amount of value-added tax. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) Where a qualifying contractor receives payment from the individual in respect of qualifying work to which this section applies on or after 25 October 2013 and before the electronic systems referred to in subsection (10) are made available by the Revenue Commissioners, that contractor shall provide to the Revenue Commissioners the information specified in paragraph (a) within 28 days of such electronic systems being made available. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(6) On making a claim under this section, the claimant shall provide to the Revenue Commissioners— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) the following information: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) his or her name and tax reference number; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) the unique reference number for the work; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iii) the unique identification number assigned in accordance with section 27 of the Finance (Local Property Tax) Act 2012 to the property on which the qualifying work was carried out; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iv) details of any sum referred to in paragraph (a) or (b) of subsection (7), | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) a declaration (unless the contrary is the case) in respect of each such payment that— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) the amount of the payment advised to the Revenue Commissioners by the qualifying contractor under subsection (5)(a)(i)(IV) accords with the amount of the payment made by the claimant to that contractor, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) the date of the payment advised to the Revenue Commissioners by the qualifying contractor under subsection (5)(a)(i)(V) is correct, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iii) the work in respect of which payment was made to the qualifying contractor was qualifying work carried out on the claimant’s qualifying residence, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iv) the work in respect of which payment was made to the qualifying contractor has been completed, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(v) the contractor has received full payment from the claimant in respect of the work, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(vi) the property on which the qualifying work was carried out was occupied by the individual as his or her only or main residence on completion of the work. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(7) Where a claimant has received or will receive, in respect of, or by reference to, qualifying work, a sum directly or indirectly— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) from the State or any public body or local authority, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) under any contract of insurance or by way of compensation or otherwise, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

then, for the purposes of subsection (3)(a), the amount of any payment or payments, as specified in the information provided to the Revenue Commissioners under subsection (5), made in respect of qualifying expenditure on that qualifying work shall be reduced— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) in the case of paragraph (a), by an amount equal to 3 times the sum received or receivable, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) in the case of paragraph (b), by an amount equal to the sum received or receivable. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(8) (a) Relief shall not be given under this section where the requirements of the Finance (Local Property Tax) Act 2012 , in relation to the making of returns and the payment of local property tax— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) have not been complied with in respect of the qualifying residence, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) have not been complied with by a claimant in respect of any relevant residential property (other than the qualifying residence) in relation to which the claimant is a liable person. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) In this subsection ‘relevant residential property’ and ‘liable person’ have the same meanings respectively as in the Finance (Local Property Tax) Act 2012 . | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(9) For the purposes of this section— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in the case of a claimant assessed to tax for a year of assessment in accordance with section 1017, any payment in respect of qualifying expenditure to a qualifying contractor made by the claimant’s spouse, in respect of which the claimant’s spouse would have been entitled to relief under this section if that spouse were assessed to tax for the year of assessment in accordance with section 1016 (apart from subsection (2) of that section), shall be deemed to have been made by the claimant, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in the case of a nominated civil partner assessed to tax for a year of assessment in accordance with section 1031C, any payment in respect of qualifying expenditure to a qualifying contractor made by the other civil partner, in respect of which the other civil partner would have been entitled to relief under this section if the other civil partner were assessed to tax for the year of assessment in accordance with section 1031B (apart from subsection (2) of that section), shall be deemed to have been made by the nominated civil partner. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(10) Any claim, notification, information or declaration required by this section shall be given by electronic means and through such electronic systems as the Revenue Commissioners may make available for the time being for any such purpose, and the relevant provisions of Chapter 6 of Part 38 shall apply. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(11) Where qualifying expenditure, in relation to qualifying work on a qualifying residence, is incurred by 2 or more claimants, then, except where subsection (9) applies, for the purposes of apportioning the specified amount, each claimant shall be entitled to an amount which bears the same proportion to the specified amount as the qualifying expenditure incurred by that claimant on the qualifying residence bears to the total qualifying expenditure incurred on that residence. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(12) Expenditure in respect of which a claimant is entitled to relief under this section shall not include any expenditure in respect of which that claimant is entitled to a deduction, relief or allowance under any other provision of the Tax Acts or the Value-Added Tax Consolidation Act 2010 . | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(13) Anything required to be done by or under this section by the Revenue Commissioners, other than the making of regulations, may be done by any Revenue officer. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(14) (a) The Revenue Commissioners may make regulations for the purposes of this section and those regulations may— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) specify the manner in which contractors shall provide to the Revenue Commissioners the information required under subsections (4) and (5), | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) specify the manner in which a claimant shall provide to the Revenue Commissioners the information and declaration required under subsection (6), | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iii) specify the manner in which the Revenue Commissioners shall issue notifications under subsection (4)(b)(ii), and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iv) provide for such other matters relating to the information required under subsections (4)(a) and (5)(a) and to the information and declaration required under subsection (6) as are considered necessary and appropriate by the Revenue Commissioners for the purposes of this section and as may be specified in the regulations. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) Regulations made under this section may contain such incidental, supplemental or consequential provisions as appear to the Revenue Commissioners to be necessary or expedient— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) to enable persons to fulfil their obligations under this section or under regulations made under this section, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) to give effect to the proper implementation and efficient operation of the provisions of this section or regulations made under this section. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) Regulations made under this section shall be laid before Dáil Éireann as soon as may be after they are made and, if a resolution annulling those regulations is passed by Dáil Éireann within the next 21 days on which Dáil Éireann has sat after the regulations are laid before it, the regulations shall be annulled accordingly, but without prejudice to the validity of anything previously done under them.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in Schedule 29, in column 3, by inserting “section 477B” after “section 267B”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Relief for long-term unemployed starting a business | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

6. Chapter 1 of Part 15 of the Principal Act is amended by inserting the following after section 472A: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“472AA. (1) In this section— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘Act of 2005’ means the Social Welfare Consolidation Act 2005 ; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘basis period’, in relation to a year of assessment, means the period on the profit or gains of which income tax for the year of assessment is to be finally computed under the Income Tax Acts; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘continuous period of unemployment’ has the meaning assigned to it in section 141(3) of the Act of 2005; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘crediting contribution’ means a crediting contribution provided for by regulations made under section 33 of the Act of 2005; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘new business’ means a trade or profession which is set up and commenced by a qualifying individual during the period beginning on 25 October 2013 and ending on 31 December 2016, other than a trade or profession— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) which was previously carried on by another person and to which the qualifying individual has succeeded, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) the activities of which were previously carried on as part of another person’s trade or profession; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘qualifying individual’ means an individual who commences a new business and— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) who— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) has been continuously unemployed for the period of 12 months immediately preceding the commencement of that business, and in respect of that period of unemployment, was entitled to crediting contributions, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) in respect of a continuous period of unemployment of not less than 312 days immediately preceding the commencement of that business, has been in receipt of— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(I) jobseeker’s benefit under Chapter 12 of Part 2 of the Act of 2005, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(II) jobseeker’s allowance under Chapter 2 of Part 3 of the Act of 2005, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(III) one-parent family payment under Chapter 7 of Part 3 of the Act of 2005, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(IV) partial capacity payment under Chapter 8A of Part 2 of the Act of 2005, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) who was not previously a qualifying individual for the purposes of this section; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘qualifying period’ means a period of 24 months beginning on the date the qualifying individual commenced a new business; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘unemployment payment’ means a payment of jobseeker’s benefit or jobseeker’s allowance payable under the Social Welfare Acts. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(2) For the purposes of the definition of ‘qualifying individual’ in subsection (1)— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) any period where an individual is in attendance at, or participating in, a scheme or programme of employment or work experience, or a course of education, training or development, where such a scheme, programme or course is approved for the purposes of this paragraph by the Minister for Social Protection or the Minister for Education and Skills, with the consent of the Minister for Finance, shall be deemed to be part of a continuous period of unemployment for the purposes of this section, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) any payment in respect of a period of attendance at, or participation in, a scheme, programme or course mentioned in paragraph (a) shall be deemed to be an unemployment payment for the purposes of this section if the qualifying individual concerned was in receipt of an unemployment payment immediately prior to the commencement of such period, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) any Sunday in any period of consecutive days shall not be treated as a day of unemployment and shall be disregarded in computing any such period. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(3) Subject to this section, where, on making a claim, an individual proves that he or she is a qualifying individual, he or she shall be entitled in any year of assessment falling wholly or partly within the qualifying period to deduct from or set off against the profits or gains of the new business, on which that individual is assessed under Case I or Case II of Schedule D, an amount equal to the amount referred to in subsection (4). | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

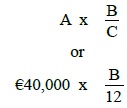

(4) The amount to which subsection (3) refers is an amount equal to the lesser of— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

where— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

A is the profit or gains of the new business which would, but for this section, be charged to tax in the year of assessment, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

B is the number of months or fractions of months within the year of assessment which fall within the qualifying period, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

C is the number of months or fractions of months in the basis period for the year of assessment. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(5) Notwithstanding any other provision of the Tax Acts, effect shall be given to a deduction or set-off under subsection (4) in priority to any relief under section 382 and any allowance made in respect of the new business in accordance with Part 9. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(6) Where a qualifying individual commences 2 or more new businesses, the total deduction available under this section shall not exceed €40,000 for a year of assessment. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(7) Notwithstanding any other provision of the Tax Acts, an individual who makes a claim under this section shall be a chargeable person within the meaning of section 959A.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Single person child carer credit | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

7. (1) The Principal Act is amended— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in section 3, in the definition of “personal tax credit”, by substituting “462B” for “462”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in section 7(2) by substituting “section 462B” for “section 462”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) in section 15(2)(b) by substituting “section 462B” for “section 462”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(d) in section 188(2A)(b) by substituting “section 462B, but without regard to subsections (1)(b), (1)(c), (3) and (5)” for “section 462, but without regard to subsections (1)(b), (2) and (3)”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(e) in Part 2 of the Table to section 458 by substituting “Section 462B” for “Section 462”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(f) in section 461A by substituting “section 462B” for “section 462”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(g) in section 462 by inserting the following subsection after subsection (5): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(6) This section shall cease to apply for the year of assessment 2014 and subsequent years of assessment.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(h) by inserting the following section before section 463: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Single person child carer credit | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

462B. (1) (a) In this section— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘order’, in relation to a child, means an order made by the court under section 11 of the Guardianship of Infants Act 1964 granting custody of the child to the child’s father and mother jointly; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘qualifying child’ in relation to any primary claimant and year of assessment means a child— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) who is born in the year of assessment, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) who, at the commencement of the year of assessment, is under the age of 18 years, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iii) who, if over the age of 18 years at the commencement of the year of assessment— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(I) is receiving full-time instruction at any university, college, school or other educational establishment, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(II) is permanently incapacitated by reason of mental or physical infirmity from maintaining himself or herself and had become so permanently incapacitated before he or she had attained the age of 21 years or had become so permanently incapacitated after attaining the age of 21 years but while he or she had been in receipt of such full-time instruction, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and who— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(A) is a child of the primary claimant, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(B) not being such a child is in the custody of the primary claimant, and is maintained by the primary claimant at the primary claimant’s own expense for the whole or the greater part of the year of assessment or, in respect of a child born in the year of assessment, for the greater part of the period remaining in that year of assessment from the date of birth of that child. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) This section shall apply to an individual who is not entitled to a basic personal credit referred to in paragraph (a) or (b) of section 461. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) This section shall not apply for any year of assessment— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) in the case of either party to a marriage unless— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(I) the parties are separated under an order of a court of competent jurisdiction or by deed of separation, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(II) they are in fact separated in such circumstances that the separation is likely to be permanent, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) in the case of either civil partner in a civil partnership unless the civil partners are living separately in circumstances where reconciliation is unlikely, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iii) in the case of cohabitants. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(2) (a) This paragraph applies to an individual (in this section referred to as the ‘primary claimant’), being an individual to whom this section applies, who proves for a year of assessment that a qualifying child is resident with him or her for the whole or the greater part of that year of assessment or, in respect of a child born in that year of assessment, for the greater part of the period remaining in that year of assessment from the date of birth of that child, provided that where a child is the subject of an order and the child resides with each parent for an equal part of the year of assessment, this paragraph shall apply to whichever of the parents referred to in that order is the recipient of the child benefit payment made under Part 4 of the Social Welfare Consolidation Act 2005 . | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) This paragraph applies to an individual (in this section referred to as the ‘secondary claimant’), being an individual to whom this section applies, who proves for a year of assessment that a qualifying child of a primary claimant is resident with him or her for a period of, or periods that in aggregate amount to, not less than 100 days. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(3) Subject to subsection (5), an individual to whom subsection (2)(a) applies, shall be entitled to a tax credit (in this section referred to as a ‘single person child carer credit’) of €1,650. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(4) Subject to subsection (5), and notwithstanding subsection (3), where for any year of assessment a primary claimant would be entitled to a single person child carer credit but for the fact that he or she has, in the form specified by the Revenue Commissioners, relinquished his or her claim to that credit, a secondary claimant shall be entitled to claim a single person child carer credit in respect of the qualifying child concerned. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(5) A claimant under this section shall be entitled to only one single person child carer credit for any year of assessment irrespective of the number of qualifying children resident with the claimant in that year. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(6) (a) The references in subsection (1)(a) to a child receiving full-time instruction at an educational establishment shall include references to a child undergoing training by any person (in this subsection referred to as ‘the employer’) for any trade or profession in such circumstances that the child is required to devote the whole of his or her time to the training for a period of not less than 2 years. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) For the purpose of a claim in respect of a child undergoing training, the inspector may require the employer to furnish particulars with respect to the training of the child in such form as may be prescribed by the Revenue Commissioners. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(7) Where any question arises as to whether any person is entitled to a single person child carer credit in respect of a child over the age of 18 years as being a child who is receiving full-time instruction referred to in this section, the Revenue Commissioners may consult the Minister for Education and Skills. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(8) For the purposes of this section a child shall be treated as resident with an individual for any day where the child so resides for the greater part of that day.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) in section 463(1) by substituting the following for the definition of “qualifying child”: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“ ‘qualifying child’, in relation to a claimant and a year of assessment, has the same meaning as in section 462B, and the question of whether a child is a qualifying child shall be determined on the same basis as it would be for the purposes of section 462B, and subsections (5), (6) and (7) of that section shall apply accordingly.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(j) in section 1023(1) by substituting “462B” for “462”, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(k) in section 1031H(1) by substituting “462B” for “462”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(2) Paragraphs (a) to (f) and (h) to (k) of subsection (1) shall apply for the year of assessment 2014 and subsequent years of assessment. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Amendment of section 470 of Principal Act (relief for insurance against expense of illness) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

8. (1) Section 470 of the Principal Act is amended in subsection (1)— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) by inserting the following definition: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“ ‘child’ means an individual under the age of 18 years or, if over the age of 18 years and under the age of 23 years, who is receiving full-time education and in respect of whom the payment under a relevant contract has been reduced in accordance with paragraph (a)(ii) or (b)(i) of section 7 (5) of the Health Insurance Act 1994 ;”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) by substituting the following for the definition of “relevant contract”: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“ ‘relevant contract’ means a contract of insurance which provides specifically, whether in conjunction with other benefits or not, for the reimbursement or discharge, in whole or in part, of— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) actual health expenses (within the meaning of section 469), being a contract of medical insurance, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) dental expenses other than expenses in respect of routine dental treatment (within the meaning of section 469), being a contract of dental insurance;”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) by substituting the following for the definition of “relievable amount”: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“ ‘relievable amount’, in relation to a payment to an authorised insurer under a relevant contract, means— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) where the payment covers no benefits other than such reimbursement or discharge as is referred to in the definition of ‘relevant contract’, an amount equal to the full amount of the payment reduced by the amount of credit due (if any) under section 470B(4) and credit due (if any) under a risk equalisation scheme (within the meaning of the Health Insurance Act 1994 ), or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) where the payment covers benefits other than such reimbursement or discharge as is referred to in that definition, an amount equal to so much of the payment as is referable to such reimbursement or discharge reduced by the amount of credit due (if any) under section 470B(4) and credit due (if any) under a risk equalisation scheme (within the meaning of the Health Insurance Act 1994 ), | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

provided that in respect of a relevant contract renewed or entered into on or after 16 October 2013 the relievable amount in respect of any payment made under a relevant contract, in respect of any 12 month period covered by that contract, shall not exceed the aggregate of— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) the lesser of the relievable amount attributable to each individual, other than a child, to whom the relevant contract relates, or €1,000 in respect of each individual, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) the lesser of the relievable amount attributable to each child to whom the relevant contract relates, or €500 in respect of each child, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and where the contract is for a period of less than 12 months or being for a period of 12 months is terminated before the end of that period, the relievable amount shall be reduced proportionately.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(2) This section shall apply in respect of relevant contracts (within the meaning of section 470 of the Principal Act) entered into or renewed on or after 16 October 2013. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Amendment of section 469 of Principal Act (relief for health expenses) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

9. Section 469 of the Principal Act is amended in subsection (1)— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) by substituting the following for the definition of “educational psychologist”: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“ ‘educational psychologist’ means a psychologist who has expertise in the education of students;”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) by deleting the definition of “speech and language therapist”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Exemption in respect of annual allowance for reserve members of the Garda Síochána | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

10. The Principal Act is amended by inserting the following section after section 204: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“204A. The annual allowance payable under Regulation 15 of the Garda Síochána (Reserve Members) Regulations 2006 ( S.I. No. 413 of 2006 ) shall be exempt from income tax and shall not be reckoned in computing income for the purposes of the Income Tax Acts.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Benefit-in-kind: application of metric measurements | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

11. Section 6 of the Finance (No. 2) Act 2008 is amended— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in subsection (1)— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) in paragraph (b)(i) by substituting “2014” for “2009”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) in paragraph (d) by substituting “2014” for “2009”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iii) in paragraph (f)(ii) by substituting “2014” for “2009”, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iv) in paragraph (g)(ii) by substituting “2014” for “2009”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) by substituting the following for subsection (2): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(2) (a) Paragraphs (a), (b)(i), (c)(i), (c)(ii), (c)(iia) (inserted by section 159 of and Schedule 4 (5) to the Finance Act 2010 ), (d), (f) and (g) of subsection (1) shall apply as on and from 1 January 2014. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) Paragraphs (b)(ii), (c)(iii) and (e) of subsection (1) shall come into operation on such day or days as the Minister for Finance may by order or orders appoint and different days may be appointed for different purposes or different provisions.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Amendment of section 126 of Principal Act (tax treatment of certain benefits payable under Social Welfare Acts) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12. Section 126 of the Principal Act is amended by inserting the following subsection after subsection (2A): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(2B) Notwithstanding the provisions of section 112(1), where an increase in the amount of a pension to which section 112 , 113 , 117 or 157 , as the case may be, of the Social Welfare Consolidation Act 2005 applies is paid in respect of a qualified adult (within the meaning of the Acts), that increase shall be treated for all the purposes of the Income Tax Acts as if it arises to and is payable to the beneficiary referred to in those sections of that Act.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Amendment of section 472D of Principal Act (relief for key employees engaged in research and development activities) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

13. Section 472D of the Principal Act is amended— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in subsection (1), in paragraph (b) of the definition of “key employee”, by substituting “whose emoluments” for “the emoluments”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) by substituting the following for subsection (2): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(2) (a) Where, as respects an accounting period, a relevant employer surrenders an amount under section 766(2A) for the benefit of a key employee, then subject to subsection (3), on the making of a claim, that employee shall be entitled for a tax year to have the income tax charged on his or her relevant emoluments for that tax year reduced by the amount surrendered. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) The tax year referred to in paragraph (a) is the tax year following the tax year during which the accounting period, referred to in that paragraph, of the relevant employer ends. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) Notwithstanding that, for the tax year for which a claim is made under this section, an employee is no longer a key employee of the company that surrendered an amount referred to in paragraph (a) but is an employee of that company, then he or she shall be entitled to have the income tax charged on emoluments from that company for that tax year reduced by the amount so referred to.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) in subsection (3)— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) in paragraph (a)— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(I) by substituting “the employee concerned or” for “a key employee including”, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(II) by substituting “applies” for “apply”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) by substituting the following for paragraph (b): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(b) Paragraph (a) also applies where— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) paragraph (a) or (b) of subsection (4) applies, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) subsection (2) and paragraph (a) or (b) of subsection (4) apply for the same tax year.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(d) in subsection (4)(a) by substituting “emoluments from that employer” for “relevant emoluments” in each place, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(e) by substituting the following for subsection (6): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(6) No reduction in income tax shall be given under this section for any tax year unless all tax deductible for that tax year from emoluments paid by the employer to the employee to whom the amount was surrendered has been remitted by that employer to the Collector- General in accordance with regulations made under Chapter 4 of Part 42.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(f) by deleting subsections (7) and (8), and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(g) in subsection (9) by substituting “an individual makes a claim for relief under this section or has the income tax charged on his or her emoluments reduced as a consequence of a claim under this section” for “an individual makes a claim for relief under this section”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Amendment of section 473A of and Schedule 29 to Principal Act (relief for fees paid for third level education, etc.) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

14. The Principal Act is amended— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in section 473A— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) by substituting the following for subsection (4): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(4) For the purposes of this section, a payment in respect of qualifying fees shall be regarded as not having been made in so far as any sum in respect of, or by reference to, such fees— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) has been or is to be received, directly or indirectly, by the individual or, as the case may be, the person by whom the course is being, or was, undertaken, from any source whatever by means of grant, scholarship or otherwise, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) is refunded or partly refunded by an approved college.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) by inserting the following after subsection (9): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(10) Where any fees that are the subject of a claim for relief under this section are refunded or partly refunded by an approved college, it shall be the duty of the individual by whom the claim is made to notify the Revenue Commissioners within 21 days of receipt of such refund that the refund has been received.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in Schedule 29, in column 3, by inserting “section 473A” after “section 267B”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Amendment of section 480A of Principal Act (relief on retirement for certain income of certain sportspersons) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

15. (1) Section 480A of the Principal Act is amended— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) by substituting the following for subsections (1) to (4): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(1) In this section— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘basis period’, in relation to a year of assessment, means the period on the profits or gains of which income tax for the year of assessment is to be finally computed under the Income Tax Acts; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘EEA Agreement’ means the Agreement on the European Economic Area signed at Oporto on 2 May 1992, as adjusted by all subsequent amendments to that Agreement; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘EEA state’ means a state, other than the State, which is a contracting party to the EEA Agreement; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘EFTA state’ means a state, other than an EEA state, which is a member of the European Free Trade Association; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘relevant individual’ means an individual who— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) engaged in a specified occupation or carried on a specified profession, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) complied with the Income Tax Acts, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) is resident in the State, an EEA state or an EFTA state in the retirement year; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘relevant period’ means the retirement year and the 14 years of assessment immediately preceding the retirement year; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘relevant years’ means the years of assessment as specified by the relevant individual, not exceeding 10 years of assessment, in the relevant period; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘retirement year’ means the year of assessment in respect of which the relevant individual proves to the satisfaction of the Revenue Commissioners that he or she has, in that year of assessment, ceased permanently to be engaged in a specified occupation or to carry on a specified profession; | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

‘specified occupation’ and ‘specified profession’ mean an occupation or profession, as the case may be, specified in Schedule 23A. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(2) Notwithstanding any other provision of the Income Tax Acts other than section 960H, this section applies to a relevant individual who ceased permanently to be engaged in a specified occupation or to carry on a specified profession. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(3) Where this section applies, the relevant individual shall, on the making of a claim in that behalf, within 4 years from the end of the retirement year, be entitled to have deductions made from his or her total income for the relevant years. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(4) (a) Subsection (3) shall apply notwithstanding any limitation in section 865(4) on the time within which a claim for a repayment of tax is required to be made. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) Section 865(6) shall not prevent the Revenue Commissioners from repaying an amount of tax as a consequence of a timely claim for relief under this section where a valid claim for a repayment of tax (within the meaning of section 865(1)(b)) has been made.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) by substituting the following for subsection (7): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(7) A claim under this section shall be made— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) where the relevant individual is required to submit a return of income in the retirement year, by including a claim in the return of income, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) where the relevant individual is not required to submit a return of income in the retirement year, by submitting a claim to the Revenue Commissioners.”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(2) Subsection (1) applies in respect of retirements on or after 1 January 2014 from occupations or professions, as the case may be, specified in Schedule 23A to the Principal Act. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Limitation on amount of certain reliefs used by certain high income individuals | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

16. The Principal Act is amended— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in Schedule 25B— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) in the matter set out opposite reference number 47A by substituting “section 490, where the subscription for eligible shares is made on or before 15 October 2013 or on or after 1 January 2017” for “section 490”, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) by inserting the following after the matter set out opposite reference number 15B: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in section 485C by inserting the following after subsection (1A): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(1B) (a) For the purposes of this subsection and Schedule 25B ‘specified plant and machinery’ means plant and machinery on which a wear and tear allowance may be granted under section 284, whether by virtue of section 298 or otherwise, which would be restricted by section 403(3) save for the provisions of section 403(9). | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) Subject to paragraph (d), a wear and tear allowance granted under section 284, or deemed to have been made to an individual under section 287, whether by virtue of section 298 or otherwise, shall only be a specified relief to the extent it relates to specified plant and machinery. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) Subject to paragraph (d), a balancing allowance arising under section 288 shall only be a specified relief to the extent it relates to specified plant and machinery. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(d) This subsection and the matters set out opposite reference numbers 15C and 15D in Schedule 25B shall not apply to allowances granted to an individual who in respect of the trade to which the allowances relate is an active trader, within the meaning of section 409D, or an active partner, within the meaning of section 409A.”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(c) in section 485FB(5)— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) by substituting “section 1016 or 1023” for “section 1016”, and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) by substituting “section 1031B or 1031H” for “section 1031B”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(d) in section 485G(4)(a) by substituting “paragraph (b), subsection (5) and paragraph 5 of Schedule 24” for “paragraph (b) and subsection (5)”. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Professional services withholding tax | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

17. (1) Chapter 1 of Part 18 of the Principal Act is amended— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) in section 521 by substituting the following for subsection (2): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(2) Where any of the persons specified in Schedule 13 is a body corporate, ‘accountable person’ includes— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(a) any subsidiary of that body corporate where such subsidiary is resident in the State and, for the purposes of this subsection, ‘subsidiary’ has the meaning assigned to it by section 155 of the Companies Act 1963 , and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) a company, resident in the State, of which more than one accountable person are members if the accountable persons— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) control the composition of its board of directors, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) hold more than half in nominal value of its equity share capital, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(iii) hold more than half in nominal value of its shares carrying voting rights (other than voting rights which arise only in specified circumstances).”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(b) in section 522 by substituting the following for paragraph (a): | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

“(a) the insurer shall, subject to section 529A, discharge the claim by making payment to the extent of the amount of the benefit, if any, due under the contract— | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(i) to the practitioner who provided the professional services to the subscriber or member concerned to whom the relevant medical expenses relate, or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

(ii) to the employer of the practitioner who provided the professional services to the subscriber or member concerned, where the professional services to which the claim relates were provided by the practitioner in the practitioner’s capacity as employee rather than on the practitioner’s own account, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and”, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

and | ||||||||||||||||||||||||||||||||||||||||||||||||||||||