| |

I, Michael Ahern, Minister of State at the Department of Enterprise, Trade and Employment, in exercise of the powers conferred on me by

section 396

of the

Companies Act 1963

(No. 33 of 1963), as adapted by the Enterprise and Employment (Alteration of Name of Department and Title of Minister) Order 1997 (

S.I. No. 305 of 1997

) and the Enterprise, Trade and Employment (Delegation of Ministerial Functions) (No. 2) Order 2003 (

S.I. No. 157 of 2003

), hereby order as follows:

1. This Order may be cited as the Companies (Forms) Order 2004.

2. This Order comes into operation on 17 May 2004.

3. In this Order—

|

| |

“Act of 1963” means the

Companies Act 1963

(No. 33 of 1963);

|

| |

“Act of 2001” means the

Company Law Enforcement Act 2001

(No. 28 of 2001);

|

| |

“used” means, in relation to a form, used and then delivered to the registrar of companies for filing.

4. Subject to Article 5 of this Order, the form (Form B1) as set out in Schedule 1 to this Order is prescribed as the form to be used for the purposes of section 125 (as inserted by section 59 of the Act of 2001) of the Act of 1963.

5. Notwithstanding Article 4 of this Order, the form (Form B1, version 2) set out in Schedule 2 to this Order is prescribed as a form which may at the option of the company concerned be used for the purposes of the said section 125 up to and including 31 October 2004.

6. The Companies (Forms) Order 2003 (

S.I. No. 189 of 2003

) is revoked.

|

| |

SCHEDULE 1

|

| | |

|

|

Companies Registration Office

|

|

Annual return

|

CRO receipt date stamp

|

|

Sections 125, 127, 128 Companies Act 1963

|

|

Section 7 Companies (Amendment) Act 1986

|

|

|

Section 26 Electoral Act 1997

|

|

Sections 43, 44 Companies (Amendment)(No. 2) Act 1999

|

|

Section 249A Companies Act 1990 (inserted by section 107 Company Law Enforcement Act 2001)

|

|

Companies Act 1990 (Form and Content of Documents Delivered to Registrar) Regulations 2002

|

|

| |

|

| |

|

| |

|

| |

|

| |

NOTES ON COMPLETION OF FORM B1

|

| |

These notes should be read in conjunction with the relevant legislation.

|

| | |

General

|

This form must be completed correctly, in full and in accordance with the following notes. Every section of the form must be completed Where “not applicable”, “nil” or “none” is appropriate, please state. Where €_ appear, please insert/delete as appropriate. Where applies, give the relevant currency, if not euro. Where the space provided on Form B1 is considered inadequate, the information shouk be presented on a continuation sheet in the same format as the relevant section in the form. The use of a continuation sheet must be so indicated in the relevant section.

|

|

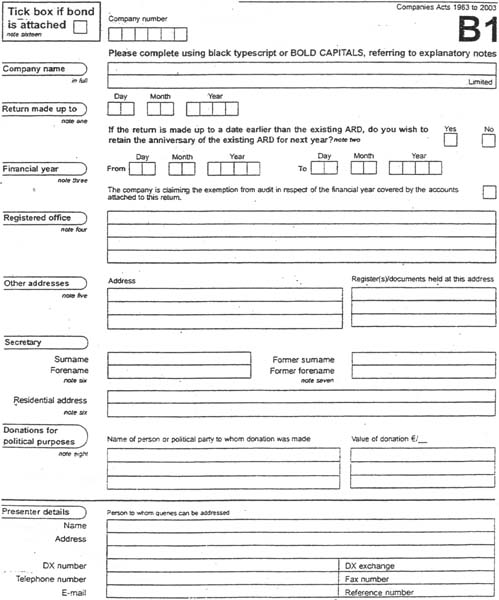

note one

|

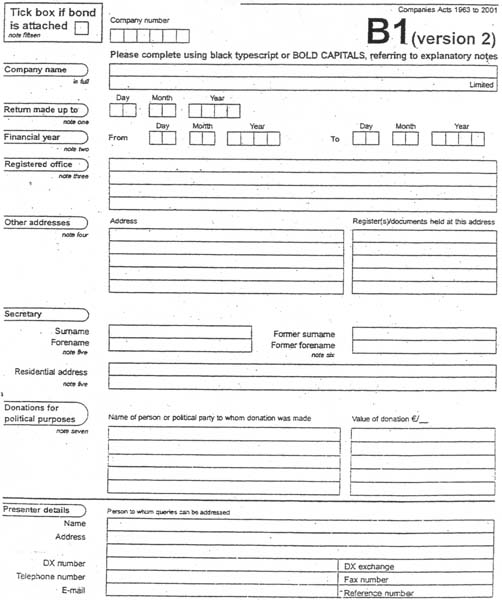

A company is required to file with this return any returns that may be outstanding in respect of previous years. There must be no gap between the effective date of the previous year’s return (if applicable) and the period covered by this return, Pursuant to s127 Companies Act 1963 a company’s return must be made up to a date not later than its Annual Return Date (ARD). However, a new company filing its first return post-incorporation must make that return up to its ARD. The return must be filed with the Registrar within 28 days of the company’s ARD or, where the return has been made up to a date earlier than the company’s ARD, within 28 days of that earlier date. S127 sets out the manner in which a company’s ARD is determined and in which it may be altered. There are severe penalties for late filing of the return Returns made up to a date prior to 1 March 2002: If this form is being used to file such a return, the return ought to be made up to the date which was 14 days after the company’s AGM for the year in question and was required to have been delivered to the CRO within 60 days of the AGM. All other notes are also applicable to such returns. The late filing penalty will be charged in respect of any such return.

|

|

note two

|

This section must be completed if this return is being made up to a date earlier than the company’s existing ARD. Where the company elects to retain the anniversary of its existing ARD for next year, the “Yes” box must be ticked. Where it elects that its ARD in the following year will be the anniversary of the date to which this return is made up, the “No” box must be ticked. If neither box is ticked, the form will be returned for correction. This section does not apply to a new company filing its first return post-incorporation.

|

|

note three

|

(i) If the return is filed with Form B73, or it is the first return of a company incorporated since 1 March 2002, no accounts need be attach and financial year details are not required. Otherwise, give the date of the commencement and completion of the financial year cover by the accounts presented or to be presented to the AGM of the company for that year. Pursuant to s7(1A) Companies (Amendment) Act 1986 (inserted by s64 Company Law Enforcement Act 2001), the accounts must be made up to a date not earlier by more than time months than the date to which the return is made up. In the case of the first return since the company’s incorporation, the period since incorporation is required to be covered by the accounts. In any other case, the accounts are required to cover the period since the last of accounts filed with the CRO.

(ii) Certain unlimited companies are required to prepare accounts and annex them to Form B1: Unlimited companies and partnerships where all the members, who do not have a limit on their liabilities, are companies limited by shares or guarantee, or their equivalent if not cover by the laws of the State, or a combination of these undertakings; unlimited companies and partnerships where all the members, who not have a limit on their liabilities, are themselves unlimited companies or partnerships of the type aforementioned that are governed the laws of the State or equivalent bodies governed by the laws of an EU Member State or combinations of these undertakings. Unlimited companies which do not come under either of these categories do not have to file accounts nor give details of their financial year.

(iii) To avail of an audit exemption, certain conditions must be satisfied. For further information see CRO Information Leaflet No. 10.

(iv) Private unlimited companies, private not-for-profit companies and certain companies with charitable objects, while exempt from anne accounts to Form B1, are required by s128(6B) Companies Act 1963 to annex a special auditor’s report to Form

|

|

note four

|

Give the address at the date of this return. Any change of registered office must be notified to the CRO. Form B2 ought to be used for this purpose.

|

|

note five

|

If not kept at the registered office, state the address(es) where the register of members, register of debenture holders, and register of directors’ and secretary’s interests in shares and debentures of the company are kept, and where copies of directors’ service contracts/memoranda of same (if applicable) are retained. Where the records are retained at an accessible website, the CRO should be notified of the relevant website address.

|

|

note six

|

Insert the full name (initials will not suffice) and usual residential address. Where the secretary is a body corporate, its company name and registered office must be stated. Where the secretary is a firm, and all the partners are joint secretaries of the company, the name and principal office of the firm will be accepted.

|

|

note seven

|

Any former forename and surname must also be stated. This does not include (a) in the case of a person usually known by a title different from his surname, the name by which he was known previous to the adoption of or succession to the title; or (b) in the case of any person, a former forename or surname where that name or surname was changed or disused before the person bearing the name attaine 18 years or has been changed or disused for a period of not less than 20 years; or (c) in the case of a married woman, the name or surname by which she was known prior to the marriage.

|

|

note eight

|

S26 Electoral Act 1997 requires details of contributions for political purposes, in excess of €5,079 in the aggregate, to any political party, member of the Dáil or Seanad, MEP or candidate in any Dáil, Seanad or European election, made by the company in the year to the annual return relates (i.e. the period since the effective date of the previous year’s annual return, up to and including the effective of the current return), to be declared in the annual return and directors’ report of the company in respect of that year. The particular be sufficient to identify the value of each such donation and the person to whom the donation was made. A wide definition of donation set out in s22/s46 of the 1997 Act and includes services supplied without charge, a donation of property or goods, or the free use of

|

|

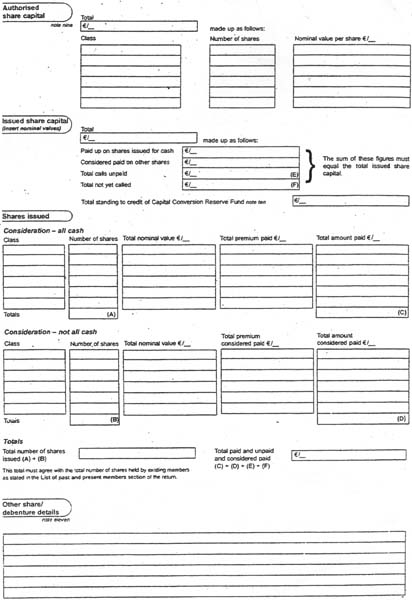

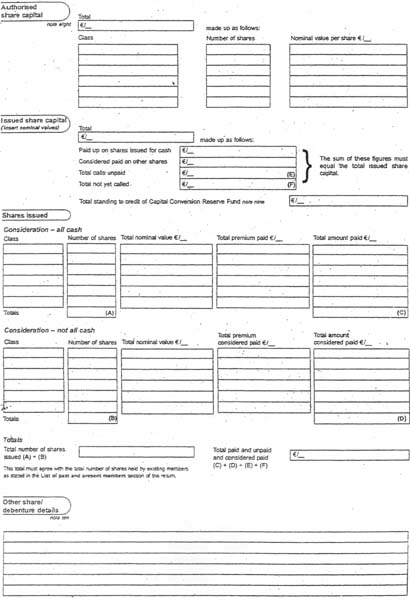

note nine

|

Where a company has converted any of its shares into stock, then, where appropriate, the references to shares shall be taken as references to stock and references to number of shares shall be taken as references to amount of stock. The second page does no to a guarantee company without a share capital.

|

|

note ten

|

insert, where applicable. (If share capital has been renominalised pursuant to s25 Economic and Monetary Union Act 1998 and there has been a decrease in the whole or part of the authorised and issued share capital or in a class of shares as a result of the renominalisation (26(4)(ka).)

|

|

note eleven

|

Details of shares forfeited, shares/debentures issued at a discount, or on which a commission was paid including share class number of shares and amounts in each case.

|

|

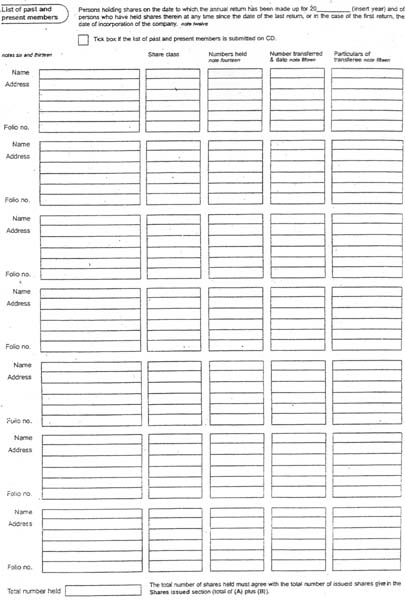

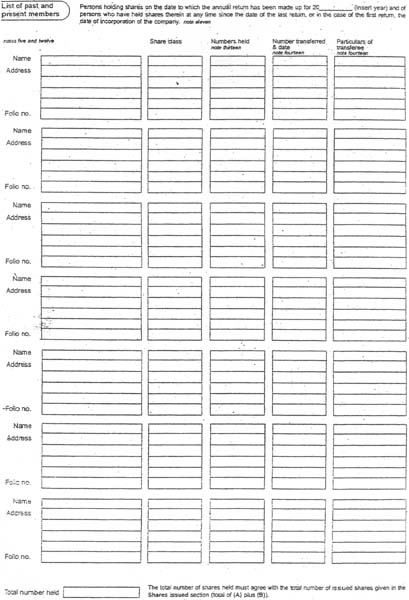

note twelve

|

A full list is required with all returns. However, this requirement does not apply to a guarantee company without a share capital. Where joint shareholders exist, name either all joint shareholders or the first shareholder and “Another”.

|

|

note thirteen

|

Where there are more than seven shareholders, the list should be given on a continuation sheet in alphabetical order

|

|

note fourteen

|

Give the total number of shares held by each member.

|

|

note fifteen

|

Applicable to private companies only. Furnish particulars of shares transferred, the date of registration of each transfer and the number of shares transferred on each date since the date of the last return, or in the case of the first return, of the incorporation of the company, by persons who are still members and persons who have ceased to be members.

|

|

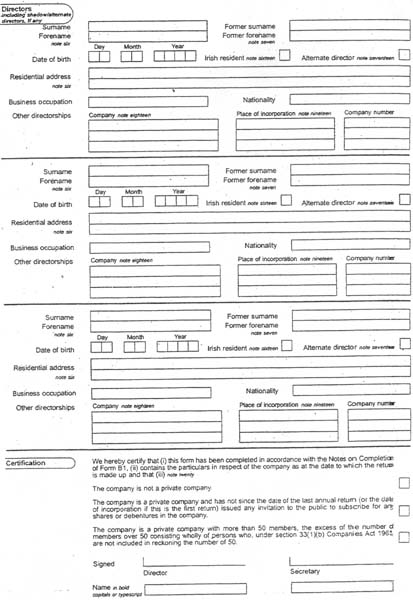

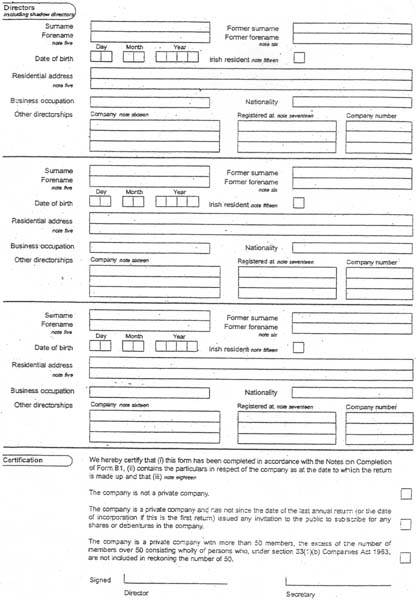

note sixteen

|

Every company must have at least one full-time Irish resident director or a bond or certificate in place pursuant to s43(3) and s44 Companies (Amendment)(No.2) Act 1999, Note that an Irish resident alternate director is not sufficient for the purposes of s43. Place a tick in the “Irish resident” box if the director is resident in the State in accordance with s43 of the 1999 Act as defined by s44(8) and (9) of that Act. If no full-time director is so resident and no certificate has been granted, a valid bond must be furnished with the return, unless same has already been delivered to the CRO on behalf of the company. (Please note that “Irish resident” means resident in the Republic of Ireland.) For further information see CRO Information Leaflet No. 17.

|

|

note seventeen

|

Please tick the box if the director is an alternate (substitute) director. If the company’s articles so permit and subject to compliance with those articles, a director may appoint a person to be an alternate director on his/her behalf. The appointment of any person to act as director is notifiable by a company to the CRO, regardless of how the appointment is described. The company is statutorily obliged to notify the CRO of the addition to and removal of each person from its register. In the event that a full-time director who has appointed an alternate director ceases to act as director, the company is required to notify the CRO of the termination of appointment of the full-time director and of his/her alternate. Note: The CRO accepts no responsibility for maintaining the link between a full-time director and his/her alternate.

|

|

note eighteen

|

Company name and number of other bodies corporate, whether incorporated in the State or elsewhere, except for bodies (a) of which the person has not been a director at any time during the past ten years; (b) of which the company is (or was at the relevant time) a wholly owned subsidiary; or (c) which are (or were at the relevant time) wholly owned subsidiaries of the company. Pursuant to s45(1) Companies (Amendment)(No.2) Act 1999, a person shall not at a particular time be a director of more than 25 companies. However, under s45(3), certain directorships are not reckoned for the purposes of s45(1).

|

|

note nineteen

|

Place of incorporation if outside the State.

|

|

note twenty

|

Tick the relevant box(es).

|

|

|

|

| |

SCHEDULE 2

|

| | |

|

|

Companies Registration Office

|

|

Annual return

|

CRO receipt date stamp

|

|

Sections 125, 127, 128 Companies Act 1963

|

|

Section 7 Companies (Amendment) Act 1986

|

|

|

Section 26 Electoral Act 1997

|

|

Sections 43, 44 Companies (Amendment)(No. 2) Act 1999

|

|

Section 249A Companies Act 1990 (inserted by section 107 Company Law Enforcement Act 2001)

|

|

Companies Act 1990 (Form and Content of Documents Delivered to Registrar) Regulations 2002

|

|

| |

|

| |

|

| |

|

| |

|

| |

NOTES ON COMPLETION OF FORM B1

|

| |

These notes should be read in conjunction with the relevant legislation.

|

| | |

General

|

This form must be completed correctly, in full and in accordance with the following notes. Every section of the form must be completed. Where “not applicable”, “nil” or “none” is appropriate, please state. Where €_ appear, please insert/delete as appropriate. Where €_ applies, give the relevant currency, if not euro. Where the space provided on Form B1 is considered inadequate, the information should be presented on a continuation sheet in the same format as the relevant section in the form. The use of a continuation sheet must be so indicated in the relevant section.

|

|

note one

|

A company is required to file with this annual return any annual returns that may be outstanding in respect of previous years. There must be no gap between the effective date of the previous year’s annual return (if applicable) and the period covered by this return. Returns made up to a date on or after 1 March 2002: Pursuant to section 127 Companies Act 1963 (inserted by section 60 Company Law Enforcement Act 2001), a company’s annual return must be made up to a date not later than its annual return date (ARD). The return must be filed with the Registrar within 28 days of the company’s ARD, or, where the return has been made up to a date earlier than the company’s ARD, within 28 days of that earlier date. Section 127 sets out the manner in which a company’s ARD is determined and in which it may be altered: There are severe penalties for late filing of the annual return. Returns made up to a date prior to 1 March 2002: If this form is being used to file such a return, the return ought to be made up to the date which is 14 days after the company’s AGM for the year in question and delivered to the CRO within 60 days of the AGM. All other notes are also applicable to such returns. The late filing penalty will be charged in respect of any such return which is delivered more than 77 days after the date to which it has been made up.

|

|

note two

|

If the return is filed with Form B73 or Form B73(a), or It is the first annual return of a company incorporated since 1 March 2002, no accounts need be attached and financial year details are not required. Otherwise, give the date of the commencement and completion of the financial year covered by the accounts presented or to be presented to the AGM of the company for that year. Pursuant to section 7(1A) Companies (Amendment) Act 1986 (inserted by section 64 Company Law Enforcement Act 2001), the accounts must be made up to a date not earlier by more than nine months than the date to which the annual return is made up. In the case of the first annual return since the company’s incorporation, the period since incorporation is required to be covered by the accounts. In any other case, the accounts are required to cover the period since the last set of accounts filed with the CRO.

Certain unlimited companies are required to prepare accounts and annex them to Form B1: Unlimited companies and partnerships where all the members, who do not have a limit on their liabilities, are companies limited by shares or guarantee, or their equivalent if not covered by the laws of the State, or a combination of these undertakings; unlimited companies and partnerships where all the members, who do not have a limit on their liabilities, are themselves unlimited companies or partnerships of the type aforementioned that are governed by the laws of the State or equivalent bodies governed by the laws of an EU Member State or combinations of these undertakings. Unlimited companies which do not come under either of these categories do not have to file accounts nor give details of their financial year.

|

|

note three

|

Give the address at the date of this return. Any change of registered office must be notified to the CRO. Form B2 ought to be used for this purpose.

|

|

note four

|

If not kept at the registered office, state the address(es) where the register of members, register of debenture holders, and register of directors’ and secretary’s interests in shares and debentures of the company are kept, and where copies of directors’ service contracts/memoranda of same (if applicable) are retained. Where the records are retained at an accessible website, the CRO should be notified of the relevant website address

|

|

note five

|

Insert the full name (initials will not suffice) and usual residential address. Where the secretary is a body corporate, its company name and registered office must be stated. Where the secretary is a firm, and all the partners are joint secretaries of the company, the name and principal office of the firm will be accepted.

|

|

note six

|

Any former forename and surname must also be stated. This does not include (a) in the case of a person usually known by a title different from his surname, the name by which he was known previous to the adoption of or succession to the title; or (b) in the case of any person, a former forename or surname where that name or surname was changed or disused before the person bearing the name attained age 18 years or has been changed or disused for a period of not less than 20 years; or (c) in the case of a married woman, the name or surname by which she was known prior to the marriage.

|

|

note seven

|

Section 26 Electoral Act 1997 requires details of contributions for political purposes, in excess of €5,079 in the aggregate, to any political party, member of the Dáil or Seanad, MEP or candidate in any Dáil, Seanad or European election, made by the company in the year to which the annual return relates (i.e. the period since the effective date of the previous year’s annual return, up to and including the effective date of the current return), to be declared in the annual return and directors’ report of the company in respect of that year. The particulars must be sufficient to identify the value of each such donation and the person to whom the donation was made. A wide definition of donation is set out in section 22/section 46 of the 1997 Act and includes services supplied without charge, a donation of property or goods, or the free use of same.

|

|

note eight

|

Where a company has converted any of its shares into stock, then, where appropriate, the references to shares shall be taken as references to stock and references to number of shares shall be taken as references to amount of stock. The second page does not apply to a guarantee company without a share capital.

|

|

note nine

|

Insert, where applicable. (If share capital has been renominalised pursuant to section 26 Economic and Monetary Union Act 1998 and there has been a decrease in the whole or part of the authorised and issued share capital or in a class of shares as a result of the renominalisation (section 26(4)(a).)

|

|

note ten

|

Details of shares forfeited, shares/debentures issued at a discount, or on which a commission was paid including share class, number of shares and amounts in each case.

|

|

note eleven

|

A full list is required with all returns. However, this requirement does not apply to a guarantee company without a share capital. Where joint shareholders exist, name either all joint shareholders or the first shareholder and “Another”.

|

|

note twelve

|

Where there are more than seven shareholders, the list should be given on a continuation sheet in alphabetical order.

|

|

note thirteen

|

Give the total number of shares held by each member.

|

|

note fourteen

|

Applicable to private companies only. Furnish particulars of shares transferred, the date of registration of each transfer and the number of shares transferred on each date since the date of the last return, or in the case of the first return, of the incorporation of the company, by persons who are still members and persons who have ceased to be members.

|

|

note fifteen

|

Every company must have at least one Irish resident director or a bond or certificate in place pursuant to sections 43(3) and 44 Companies (Amendment)(No.2) Act 1999. Place a tick in the “Irish resident” box if the director is resident in the State in accordance with section 43 of the 1999 Act as defined by section 44(8) and (9). If no director is so resident and no certificate has been granted, a valid bond must be furnished with the annual return, unless same has already been delivered to the CRO on behalf of the company. (Please note that “Irish resident” means resident in the Republic of Ireland.) For further information see CRO Information Leaflet No. 17.

|

|

note sixteen

|

Company name and number of other bodies corporate, whether incorporated in the State or elsewhere, except for bodies (a) of which the person has not been a director at any time during the past ten years; (b) of which the company is (or was at the relevant time) wholly owned subsidiary; or (c) which are (or were at the relevant time) wholly owned subsidiaries of the company.

Pursuant to section 45(1) Companies (Amendment)(No.2) Act 1999, a person shall not at a particular time be a director of more than 25 companies. However, under section 45(3), certain directorships are not reckoned for the purposes of section 45(1).

|

|

note seventeen

|

Place of incorporation if outside the State.

|

|

note eighteen

|

Tick the relevant box(es).

|

|

| | |

|

GIVEN under my hand, 6th April, 2004.

|

|

|

MICHAEL AHERN,

Minister of State at the Department of Enterprise Trade and Employment.

|

|

|

|

| |

EXPLANATORY NOTE.

|

| |

(This note is not part of the Instrument and does not purport to be a legal interpretation.)

|

| |

The purpose of this Order is to amend the form prescribed for the purposes of

section 125

of the

Companies Act 1963

, by introducing a new Form B1 with effect from 17 May 2004. This Form updates the form to be completed when furnishing an annual return to the Registrar of Companies. The Order further provides that the Form B1 previously in use (Form B1 (version 2), set out in the Schedule 2) may continue tinue to be used to deliver an annual return to the Registrar of Companies until 31 October 2004, and that with effect from 1 November 2004, only the version of the Form B1 set out in the Schedule 1 of this Order may be completed when furnishing an annual return to the Registrar of Companies.

|