S.I. No. 281/2010 - European Communities (Consumer Credit Agreements) Regulations 2010

ARRANGEMENT OF REGULATIONS | ||

Part 1 Preliminary | ||

1 Citation. | ||

2 Commencement. | ||

3 Scope of these Regulations. | ||

4Relationship of Parts 2 to 7 of these Regulations with Consumer Credit Act 1995. | ||

5 Effect on existing agreements. | ||

6 Interpretation. | ||

Part 2 Information and practices preliminary to conclusion of credit agreements | ||

7 Standard information to be included in advertising of credit. | ||

8 Pre-contractual information — general obligations. | ||

9Pre-contractual information requirements for certain overdraft facilities and certain other credit agreements. | ||

10 Exemptions from pre-contractual information requirements. | ||

11 Obligation to assess creditworthiness of consumers. | ||

Part 3 Database access | ||

12 Refusal of credit applications on basis of database access. | ||

Part 4 Information and rights concerning credit agreements | ||

13 Information to be included in credit agreements. | ||

14 Information concerning changes in borrowing rates. | ||

15 Obligations in relation to overdraft facilities. | ||

16 Termination of open-end credit agreements. | ||

17 Right of withdrawal. | ||

18 Linked credit agreements. | ||

19 Early repayment. | ||

20 Assignment of creditors’ rights. | ||

21 Overrunning. | ||

Part 5 Annual percentage rate of charge | ||

22 Calculation of annual percentage rate of charge. | ||

Part 6 Credit intermediaries | ||

23 Obligations of credit intermediaries. | ||

Part 7 Miscellaneous | ||

24 Anti-avoidance. | ||

25 Penalties. | ||

26 Regulation of certain friendly societies for certain purposes. | ||

Part 8 Amendments of other statutory instruments | ||

27 Amendment of Distance Marketing Regulations. | ||

Schedule 1 Methods of calculating annual percentage rate of charge | ||

Part 1Basic equation expressing equivalence of drawdowns with repayments and charges | ||

Part 2Additional assumptions for calculation of annual percentage rate of charge | ||

Schedule 2 Standard European Consumer Credit Information Form | ||

Schedule 3 European Consumer Credit Information Form for overdrafts, consumer credit offered by certain credit organisations and debt conversion | ||

EUROPEAN COMMUNITIES (CONSUMER CREDIT AGREEMENTS) REGULATIONS 2010 | ||

Notice of the making of this Statutory Instrument was published in | ||

“Iris Oifigiúil” of 11th June, 2010. | ||

I, BRIAN LENIHAN, Minister for Finance, in exercise of the powers conferred on me by section 3 of the European Communities Act 1972 (No. 27 of 1972) (as amended by the European Communities Act 2007 (No. 18 of 2007)), and for the purpose of giving effect to Directive 2008/48/EC 1 of the European Parliament and of the Council of 23 April 2008, hereby make the following regulations: | ||

PART 1 Preliminary | ||

Citation | ||

1. These Regulations may be cited as the European Communities (Consumer Credit Agreements) Regulations 2010. | ||

Commencement | ||

2. These Regulations come into operation on 11 June 2010. | ||

Scope of these Regulations | ||

3. (1) Subject to paragraphs (2) to (6), Parts 2 to 7 of these Regulations apply to credit agreements. | ||

(2) Only the following provisions of Parts 2 to 7 of these Regulations apply to a credit agreement in the form of an overdraft facility where the credit has to be repaid on demand or within 3 months: | ||

(a) the following provisions of Regulation 7: | ||

(i) paragraph (1); | ||

(ii) subparagraphs (a) to (c) of paragraph (2); | ||

(iii) paragraph (5); | ||

(b) Regulations 9 to 12; | ||

(c) the following provisions of Regulation 13: | ||

(i) paragraphs (1), (2) and (6); | ||

(ii) subparagraphs (a) to (f) and subparagraph (h) of paragraph (7); | ||

(d) Regulations 15, 18, 20, 22, 23 and 24. | ||

(3) Only Regulations 21 and 24 of Parts 2 to 7 apply to a credit agreement in the form of overrunning. | ||

(4) Subject to paragraph (5), only the following provisions of Parts 2 to 7 of these Regulations apply to a credit agreement entered into by a credit union (within the meaning given by the Credit Union Act 1997 (No. 15 of 1997)): | ||

(a) Regulations 7, 9 and 12; | ||

(b) the following provisions of Regulation 13: | ||

(i) paragraphs (1) and (2); | ||

(ii) subparagraphs (a) to (h) and subparagraph (l) of paragraph (3); | ||

(iii) paragraph (6); | ||

(c) Regulations 14 and 16; | ||

(d) Regulations 19 to 24. | ||

(5) Paragraph (4) ceases to have effect on 11 December 2011. | ||

(6) Parts 2 to 7 of these Regulations do not apply— | ||

(a) to a credit agreement secured by— | ||

(i) a mortgage or another comparable security on immovable property, or | ||

(ii) a right related to immovable property, | ||

(b) to a credit agreement the purpose of which is to acquire or retain property rights in land or in an existing or projected building, | ||

(c) to a credit agreement involving a total amount of credit of less than €200 or more than €75,000, | ||

(d) subject to paragraph (7), to a hiring or leasing agreement where an obligation to purchase the object of the agreement is not laid down either by the agreement itself or by a separate agreement, | ||

(e) subject to Regulation 9(9), to a credit agreement in the form of an overdraft facility where the credit has to be repaid within one month, | ||

(f) to a credit agreement where the credit is granted free of interest and without any other charges, | ||

(g) to a credit agreement under the terms of which the credit has to be repaid within 3 months and only insignificant charges are payable, | ||

(h) to a credit agreement where the credit is granted by an employer to an employee or employees as a secondary activity free of interest or at annual percentage rates of charge lower than those prevailing on the market and not offered to the public generally, | ||

(i) to a credit agreement concluded with an investment firm (as defined in Regulation 3(1) of the European Communities (Markets in Financial Instruments) Regulations 2007 ( S.I. No. 60 of 2007 )) (in this subparagraph called “the MiFID Regulations”) or with a credit institution (as defined in Regulation 2(1) of the European Communities (Capital Adequacy of Credit Institutions) Regulations 2006 ( S.I. No. 661 of 2006 )) for the purposes of allowing an investor to carry out a transaction relating to an instrument or instruments of a kind listed in Part 3 of Schedule 1 to the MiFID Regulations, where the investment firm or credit institution is involved in the transaction, | ||

(j) to a credit agreement that is the outcome of a settlement reached in court or before another statutory authority, | ||

(k) to a credit agreement that relates to the deferred payment, free of charge, of an existing debt, | ||

(l) to a credit agreement on the conclusion of which the consumer is requested to deposit an item as security in the creditor’s safe-keeping and under which the liability of the consumer is strictly limited to the pledged item, or | ||

(m) to a credit agreement that relates to a loan granted to a member or members of a restricted public— | ||

(i) under a statutory provision with a general interest purpose, and | ||

(ii) either— | ||

(I) at lower interest rates than those prevailing on the market or free of interest, or | ||

(II) on other terms more favourable to the consumer than those prevailing on the market and at interest rates not higher than those prevailing on the market. | ||

(7) A credit agreement shall be taken to contain an obligation referred to in paragraph (6)(d) if the creditor concerned unilaterally so decides. | ||

(8) Parts 2 to 7 of these Regulations do not apply to credit agreements entered into by the following friendly societies: | ||

(a) Ardlea Credit Union Co-operative Ltd; | ||

(b) Finglas West Credit Co-operative Ltd; | ||

(c) St. Anne’s Community Credit Co-operative Ltd; | ||

(d) Artane Credit Union Co-operative Ltd. | ||

(9) The Registrar of Friendly Societies shall, at least once in every calendar year, carry out a review to determine whether the bodies mentioned in paragraph (8) continue to meet the criterion for exemption set out in Article 2(5) of Directive 2008/48/EC 2 of the European Parliament and of the Council of 23 April 2008. | ||

Relationship of Parts 2 to 7 of these Regulations with Consumer Credit Act 1995 | ||

4. (1) For the application of Part II of the Consumer Credit Act 1995 (No. 24 of 1995) (in this Regulation called “the Act of 1995”) to advertising to which Regulation 7 applies, the annual percentage rate (in that Part called “APR”) shall be determined in accordance with the definition of “annual percentage rate of charge” in Regulation 6(1) and the formulae set out in Schedule 1. | ||

(2) Subject to paragraph (4), Parts III (other than section 30(1)), IV (other than section 42) and V of the Act of 1995 do not apply in relation to a credit agreement to which Parts 2 to 7 of these Regulations apply. | ||

(3) Where a creditor communicates with a consumer or guarantor in writing, section 45 of the Act of 1995 applies to the communication. | ||

(4) Paragraph (3) does not affect the operation of any provision of Part III, IV or V of the Act of 1995 in relation to a contract of guarantee that relates to a credit agreement. | ||

(5) Nothing in this Regulation affects the operation of any provision of the Act of 1995 in relation to advertising, or a credit agreement, to which Parts 2 to 7 of these Regulations do not apply. | ||

(6) For the purposes of this Regulation, a credit agreement referred to in Regulation 3(6)(e), and a credit agreement in the form of an overrunning, shall be taken to be a credit agreement to which these Regulations apply. | ||

Effect on existing agreements | ||

5. (1) Other than as set out in paragraphs (2) to (4), Parts 2 to 7 of these Regulations do not apply to a credit agreement that is in existence when these Regulations come into operation. | ||

(2) Regulations 14, 15, 16 and 20 apply to an open-end credit agreement that is in existence when these Regulations come into operation. | ||

(3) In relation to an open-end credit agreement that is in existence when these Regulations come into operation, the creditor concerned shall provide the information referred to in Regulation 9(1)(e) to the consumer concerned on a regular basis, on paper or another durable medium. | ||

(4) Regulation 21(2) applies to an open-end credit agreement that is in existence when these Regulations come into operation. | ||

Interpretation | ||

6. (1) In these Regulations— | ||

“annual percentage rate of charge” in relation to a credit agreement means the total cost of the credit to the consumer (including, where applicable, the costs referred to in Regulation 22(2) and (3)), expressed as an annual percentage of the total amount of credit; | ||

“borrowing rate” in relation to a credit agreement means the interest rate expressed as a fixed or variable percentage applied on an annual basis to the amount of credit drawn down; | ||

“consumer” means a natural person who is acting, in the course of a transaction to which these Regulations apply, for purposes outside his or her trade, business or profession; | ||

“contravene” includes fail to comply with; | ||

“credit agreement” means an agreement under which a creditor grants or promises to grant to a consumer credit in the form of a deferred payment, loan or other similar financial accommodation, but does not include an agreement for— | ||

(a) the provision, on a continuing basis, of services, or | ||

(b) the supply of goods of the same kind, | ||

where the consumer pays for the services or goods by instalments for the duration of their provision; | ||

“credit intermediary” means a person (including a firm, within the meaning of the Partnership Act 1890 (53 & 54 Vict. c. 39)) who is not acting as a creditor and who, in the course of trade, business or profession, for a fee (whether in pecuniary form or any other form of financial consideration)— | ||

(a) presents or offers credit agreements to consumers, | ||

(b) assists consumers by undertaking, in respect of credit agreements, preparatory work other than that referred to in subparagraph (a), or | ||

(c) concludes credit agreements with consumers on behalf of creditors; | ||

“creditor” means a person who grants or promises to grant credit in the course of trade, business or profession; | ||

“Distance Marketing Regulations” means the European Communities (Distance Marketing of Consumer Financial Services) Regulations 2004 ( S.I. No. 853 of 2004 ); | ||

“durable medium” means any medium that enables a consumer to store information addressed personally to the consumer in a way that renders it accessible for future reference for a period of time adequate for the purposes of the information and allows the unchanged reproduction of the information; | ||

“European Consumer Credit Information” has the meaning given by Regulation 9(1); | ||

“European Consumer Credit Information Form” means the form set out in Schedule 3; | ||

“fixed borrowing rate” in relation to a credit agreement means— | ||

(a) a borrowing rate that a creditor and a consumer agree on in the relevant credit agreement for the entire duration of the credit agreement, or | ||

(b) each of several borrowing rates for partial periods using exclusively a fixed specific percentage; | ||

“linked credit agreement” means a credit agreement where— | ||

(a) the credit concerned serves exclusively to finance an agreement for the supply of specific goods or the provision of a specific service, and | ||

(b) subject to paragraph (3), those two agreements objectively form a commercial unit; | ||

“overdraft facility” means an explicit credit agreement by which a creditor makes available to a consumer who operates a current account with the creditor funds in excess of the current balance in the current account; | ||

“overrunning” means a tacitly accepted overdraft—that is, an overdraft where a consumer operates a current account (with or without an explicit overdraft facility) with a creditor, and without formal agreement the creditor makes available to the consumer funds in excess of— | ||

(a) the current balance in the current account, or | ||

(b) if there is an agreed overdraft facility, the agreed limit of that facility; | ||

“Standard European Consumer Credit Information” has the meaning given by Regulation 8(1); | ||

“Standard European Consumer Credit Information Form” means the form set out in Schedule 2; | ||

“total cost of the credit to the consumer” in relation to a credit agreement means all the costs that the consumer is required to pay in connection with the credit agreement and that are known to the creditor concerned, including— | ||

(a) interest, commissions, taxes and any other kind of fees, | ||

(b) where the conclusion of a service contract is compulsory to obtain the credit or to obtain it on the terms and conditions marketed, costs in respect of ancillary services relating to the credit agreement (in particular, insurance premiums); | ||

“total amount payable by the consumer” in relation to a credit agreement means the sum of the total amount of the credit and the total cost of the credit to the consumer; | ||

“total amount of credit” in relation to a credit agreement means the limit of the credit, or the total sum, made available under the credit agreement. | ||

(2) If in a credit agreement not all the applicable borrowing rates are determined, a borrowing rate shall be taken to be fixed only for any period for which the borrowing rate is exclusively determined by a fixed specific percentage agreed on at the time when the credit agreement was concluded. | ||

(3) For the purposes of subparagraph (b) of the definition of “linked credit agreement”, a commercial unit shall be taken to exist where— | ||

(a) the supplier or service provider concerned finances the credit for the consumer, | ||

(b) if the credit is financed by a third party, the creditor uses the services of the supplier or service provider in connection with the conclusion or preparation of the credit agreement, or | ||

(c) the specific goods or the provision of a specific service are explicitly specified in the credit agreement. | ||

PART 2 Information and practices preliminary to conclusion of credit agreements | ||

Standard information to be included in advertising of credit | ||

7. (1) Any advertising concerning credit agreements that indicates an interest rate or any figures relating to the cost of the credit to the consumer shall include standard information in accordance with this Regulation. | ||

(2) The standard information shall specify in a clear, concise and prominent way by means of a representative example— | ||

(a) the borrowing rate, fixed or variable or both, together with particulars of any charges included in the total cost of the credit to the consumer, | ||

(b) the total amount of credit, | ||

(c) subject to paragraph (3), the annual percentage rate of charge, | ||

(d) if applicable, the duration of the credit agreement, | ||

(e) in relation to credit in the form of deferred payment for a specific good or service, the cash price and the amount of any advance payment, and | ||

(f) if applicable, the total amount payable by the consumer and the amount of the instalments. | ||

(3) In the case of a credit agreement relating to an overdraft facility, the annual percentage rate of charge need not be provided. | ||

(4) Where the conclusion of a contract regarding an ancillary service (in particular, insurance policy) relating to the credit agreement is compulsory in order to obtain the credit or to obtain it on the terms and conditions marketed, and the cost of that service cannot be determined in advance, the obligation to enter into that contract shall also be stated in a clear, concise and prominent way, together with the annual percentage rate of charge. | ||

(5) Nothing in this Regulation affects the operation of any law that gives effect in the State to Directive 2005/29/EC 3 . | ||

Pre-contractual information — general obligations | ||

8. (1) Subject to Regulation 10, in good time before a consumer is bound by a credit agreement or an offer of credit, the creditor concerned and any credit intermediary involved shall provide the consumer with the information needed to compare different offers in order to take an informed decision on whether to conclude a credit agreement. That information (in these Regulations called the “Standard European Consumer Credit Information”) is— | ||

(a) the type of credit, | ||

(b) the name and the geographical address of the creditor and the name and geographical address of any credit intermediary involved, | ||

(c) the total amount of credit and the conditions governing its drawdown, | ||

(d) the duration of the credit agreement, | ||

(e) in relation to credit in the form of deferred payment for a specific good or service and a linked credit agreement, the good or service concerned and its cash price, | ||

(f) the following information in relation to borrowing rates: | ||

(i) the initial borrowing rate; | ||

(ii) the conditions governing the application of the initial borrowing rate; | ||

(iii) where available, any index or reference rate applicable to the initial borrowing rate; | ||

(iv) the periods, conditions and procedure for changing the borrowing rate; | ||

(v) if different borrowing rates apply in different circumstances, the information required by sub-subparagraphs (i) to (iv) for all the applicable rates, | ||

(g) the annual percentage rate of charge and the total amount payable by the consumer, illustrated by means of a representative example mentioning all the assumptions used in order to calculate that rate, | ||

(h) the amount, number and frequency of payments to be made by the consumer and, where applicable, the order in which payments will be allocated to different outstanding balances charged at different borrowing rates for the purposes of reimbursement, | ||

(i) where applicable— | ||

(i) the charges for maintaining an account or accounts recording payment transactions and drawdowns (unless the opening of any such account is optional), | ||

(ii) any charges for using a means of payment for both payment transactions and drawdowns, | ||

(iii) any other charges deriving from the credit agreement, and | ||

(iv) the conditions under which those charges may be changed, | ||

(j) where the conclusion of an ancillary service contract (in particular, an insurance policy) is compulsory to obtain the credit or to obtain it on the terms and conditions marketed, a statement of the obligation to enter into such a contract, | ||

(k) the interest rate applicable in the case of late payments and the arrangements for its adjustment, and any charges payable for default, | ||

(l) a warning of the consequences of missing payments, | ||

(m) where applicable, the sureties required, | ||

(n) a statement that there is a right of withdrawal, or that there is no such right, as the case may be, | ||

(o) a statement of the right of early repayment, and, where applicable, information concerning the creditor’s right to compensation and the way in which that compensation will be determined in accordance with Regulation 19, | ||

(p) a statement of the consumer’s right, pursuant to Regulation 12, to be informed immediately and free of charge of the result of any database consultation carried out for the purposes of assessing the consumer’s creditworthiness, | ||

(q) a statement of the consumer’s right to be supplied, on request and free of charge, with a copy of the draft credit agreement (unless the creditor is at the time of the request unwilling to conclude the credit agreement with the consumer), and | ||

(r) if applicable, a statement of the period during which the creditor is bound by the pre-contractual information. | ||

(2) A creditor and any credit intermediary involved shall provide the Standard European Consumer Credit Information on the basis of the credit terms and conditions offered by the creditor and, if applicable, the preferences expressed and information supplied by the consumer concerned. | ||

(3) The Standard European Consumer Credit Information shall be provided— | ||

(a) on paper or on another durable medium, and | ||

(b) by means of the Standard European Consumer Credit Information Form. | ||

(4) A creditor [and any credit intermediary] shall be taken to have fulfilled the information requirements in Part 2 of the Distance Marketing Regulations if the creditor and credit intermediary have supplied the Standard European Consumer Credit Information. | ||

(5) For the purposes of giving the annual percentage rate of charge and the total amount payable by a consumer where the consumer has informed the creditor concerned of one or more components of the consumer’s preferred credit (such as the duration of the credit agreement and the total amount of credit), the creditor shall take those components into account. If a credit agreement provides different ways of drawdown with different charges or borrowing rates and the creditor uses the assumption set out in point (b) of Part 2 of Schedule 1, the creditor shall indicate that other drawdown mechanisms for that type of credit agreement may result in higher annual percentage rates of charge. | ||

(6) Any additional information that the creditor provides to the consumer shall be given in a separate document that may be annexed to the Standard European Consumer Credit Information Form. | ||

(7) In the case of an agreement concluded at a consumer’s request using a means of distance communication that does not enable the Standard European Consumer Credit Information to be provided in accordance with paragraph (1) (in particular, in the case of a credit agreement concluded by means of voice telephony communications), the creditor shall provide the consumer with the full pre-contractual information using the Standard European Consumer Credit Information Form immediately after the credit agreement is concluded. | ||

(8) A creditor shall supply a consumer on request free of charge with a copy of the draft credit agreement and an appropriately completed Standard European Consumer Credit Information Form (unless at the time of the request the creditor is unwilling to conclude the credit agreement with the consumer). | ||

(9) In the case of a credit agreement under which payments made by the consumer do not give rise to an immediate corresponding amortisation of the total amount of credit, but are used to constitute capital during periods and under conditions laid down in the credit agreement or in an ancillary agreement, the Standard European Consumer Credit Information shall include a clear and concise statement that the credit agreement does not provide for a guarantee of repayment of the total amount of credit drawn down under the credit agreement, unless such a guarantee is given. | ||

(10) A creditor or credit intermediary shall provide adequate explanation to a consumer to enable the consumer to assess whether a proposed credit agreement is appropriate to his or her needs and financial situation, where appropriate by explaining— | ||

(a) the Standard European Consumer Credit Information, | ||

(b) the essential characteristics of the products proposed, and | ||

(c) the specific effects they may have on the consumer, including the consequences of default in payment by the consumer. | ||

(11) A creditor or credit intermediary that contravenes a provision of this Regulation commits an offence. | ||

Pre-contractual information requirements for certain overdraft facilities and certain other credit agreements | ||

9. (1) Subject to Regulation 10, in good time before a consumer becomes bound by a credit agreement, or an offer concerning a credit agreement, of a kind referred to in paragraph (2) or (4) of Regulation 3, the creditor concerned and any credit intermediary involved shall provide the consumer with the information needed to compare different offers in order to take an informed decision on whether to conclude the credit agreement. That information (in these Regulations called the “European Consumer Credit Information”) is— | ||

(a) the type of credit, | ||

(b) the name and geographical address of the creditor and the name and geographical address of any credit intermediary involved, | ||

(c) the total amount of credit, | ||

(d) the duration of the credit agreement, | ||

(e) the following information in relation to borrowing rates and charges: | ||

(i) the initial borrowing rate; | ||

(ii) the conditions governing the application of the initial borrowing rate; | ||

(iii) any index or reference rate applicable to the initial borrowing rate; | ||

(iv) the charges applicable from the time the credit agreement is concluded; | ||

(v) where applicable, the conditions under which those charges may be changed, | ||

(f) subject to paragraph (5), the annual percentage rate of charge, illustrated by means of representative examples mentioning all the assumptions used in order to calculate that rate, | ||

(g) the conditions and procedure for terminating the credit agreement, | ||

(h) in the case of a credit agreement referred to in Regulation 3(2), where applicable, an indication that the consumer may be requested to repay the amount of credit in full at any time, | ||

(i) the interest rate applicable in the case of late payments and the arrangements for its adjustment, and, where applicable, any charges payable for default, | ||

(j) a statement of the consumer’s right to be informed immediately and free of charge, pursuant to Regulation 12, of the result of a database consultation carried out for the purposes of assessing the consumer’s creditworthiness, | ||

(k) in the case of a credit agreement referred to in Regulation 3(2), information about the charges applicable from the time such agreements are concluded and, if applicable, the conditions under which those charges may be changed, and | ||

(l) if applicable, the period during which the creditor is bound by the pre-contractual information. | ||

(2) The creditor and any credit intermediary involved shall provide the information required by paragraph (1) on the basis of the credit terms and conditions offered by the creditor and, if applicable, the preferences expressed and information supplied by the consumer concerned. | ||

(3) The information shall be provided on paper or on another durable medium and all information shall be equally prominent. The information may be provided by means of the European Consumer Credit Information Form set out in Schedule 3. | ||

(4) A creditor shall be taken to have fulfilled the information requirements in Regulation 6 of, and Schedule 1 to, the Distance Marketing Regulations if the creditor has supplied the European Consumer Credit Information. | ||

(5) In the case of a credit agreement of the kind referred to in Regulation 3(2), the annual percentage rate of charge need not be provided. | ||

(6) In the case of a credit agreement referred to in Regulation 3(4), the European Consumer Credit Information shall include (in addition to the information required by paragraph (1))— | ||

(a) the amount, number and frequency of payments to be made by the consumer and, where appropriate, the order in which payments will be allocated to different outstanding balances charged at different borrowing rates for the purposes of reimbursement, and | ||

(b) the right of early repayment, and, where applicable, information concerning the creditor’s right to compensation and the way in which that compensation will be determined. | ||

However, if such a credit agreement falls within the scope of Regulation 3(2), only paragraphs (1) to (3) apply to it. | ||

(7) In a credit agreement of the kind referred to in paragraph (6), the description of the main characteristics shall include a specification of the duration of the credit agreement. | ||

(8) In the case of a credit agreement for an overdraft facility made by means of voice telephony communication, where the consumer requests that the overdraft facility be made available with immediate effect, the description of the main characteristics of the financial service shall include the items referred to in subparagraphs (c), (e), (f) and (h) of paragraph (1). | ||

(9) Notwithstanding Regulation 3(6)(e), paragraph (8) applies to a credit agreement in the form of an overdraft facility where the credit has to be repaid within one month. | ||

(10) Upon request, the consumer shall also be given, free of charge, a copy of the draft credit agreement containing the contractual information required by Regulation 13 in the particular case, unless at the time of the request the creditor is unwilling to conclude the credit agreement with the consumer. | ||

(11) In the case of a credit agreement concluded at the consumer’s request using a means of distance communication that does not enable information to be provided in accordance with paragraphs (1) to (3) and (6), including in the case referred to in paragraph (8), the creditor concerned shall fulfil the obligations under paragraphs (1) to (3) and (6) by providing the contractual information required by Regulation 13 in the particular case immediately after the credit agreement is concluded. | ||

(12) A creditor or credit intermediary that contravenes a provision of this Regulation commits an offence. | ||

Exemptions from pre-contractual information requirements | ||

10. (1) Regulations 8 and 9 do not apply to a supplier of goods or services acting as a credit intermediary in an ancillary capacity. | ||

(2) Paragraph (1) does not prejudice a creditor’s obligation to ensure that a consumer receives the pre-contractual information referred to in Regulations 8 and 9. | ||

Obligation to assess creditworthiness of consumers | ||

11. (1) Before concluding a credit agreement with a consumer, a creditor shall assess the consumer’s creditworthiness on the basis of sufficient information, where appropriate obtained from the consumer and, where necessary, on the basis of a consultation of the relevant database. | ||

(2) If a creditor and a consumer agree to change the total amount of credit after a credit agreement is concluded, the creditor— | ||

(a) shall update the financial information at the creditor’s disposal concerning the consumer, and | ||

(b) shall assess the consumer’s creditworthiness before agreeing to any significant increase in the total amount of credit. | ||

(3) A creditor or credit intermediary that contravenes a provision of this Regulation commits an offence. | ||

PART 3 Database access | ||

Refusal of credit applications on basis of database access | ||

12. (1) Subject to paragraph (2), if a consumer’s credit application is rejected on the basis of the consultation of a database, the creditor concerned shall inform the consumer immediately and without charge of the result of the consultation and of the particulars of the database consulted. | ||

(2) The information need not be provided if the provision of it is prohibited by another law or is contrary to objectives of public policy or public security. | ||

(3) This Regulation is without prejudice to the application of the Data Protection Acts 1988 and 2003. | ||

(4) A creditor or credit intermediary that contravenes a provision of this Regulation commits an offence. | ||

PART 4 Information and rights concerning credit agreements | ||

Information to be included in credit agreements | ||

13. (1) A credit agreement shall be drawn up on paper or on another durable medium. | ||

(2) All the parties to a credit agreement shall receive a copy of it. | ||

(3) A credit agreement shall set out in a clear and concise manner— | ||

(a) the type of credit, | ||

(b) the names and geographical addresses of the contracting parties and of any credit intermediary involved, | ||

(c) the duration of the credit agreement, | ||

(d) the total amount of credit and the conditions governing the drawdown, | ||

(e) in the cases of credit in the form of deferred payment for a specific good or service and of a linked credit agreement, the good or service concerned and its cash price, | ||

(f) the following information in relation to borrowing rates and charges: | ||

(i) the borrowing rate; | ||

(ii) the conditions governing the application of that rate; | ||

(iii) where available, any index or reference rate applicable to the initial borrowing rate; | ||

(iv) the periods, conditions and procedures for changing the borrowing rate; | ||

(v) if different borrowing rates apply in different circumstances, the information referred to in sub-subparagraphs (i) to (iv) in respect of all the applicable rates, | ||

(g) the annual percentage rate of charge and the total amount payable by the consumer, calculated at the time the credit agreement is concluded (mentioning all the assumptions used to calculate that rate), | ||

(h) the amount, number and frequency of payments to be made by the consumer and, where applicable, the order in which payments will be allocated to different outstanding balances charged at different borrowing rates for the purposes of reimbursement, | ||

(i) where capital amortisation of a credit agreement with a fixed duration is involved, a statement of the consumer’s right to receive, on request and free of charge, at any time throughout the duration of the credit agreement, a statement of account in the form of an amortisation table in accordance with paragraphs (4) and (5), | ||

(j) if charges and interest are to be paid without capital amortisation, a statement showing the periods and conditions for the payment of the interest and of any associated recurrent and non-recurrent charges, | ||

(k) where applicable, the charges for maintaining an account or accounts recording payment transactions and drawdowns, unless the opening of any such account is optional, and any charges for using a means of payment for payment transactions and drawdowns, and any other charges deriving from the credit agreement and the conditions under which those charges may be changed, | ||

(l) the interest rate applicable in the case of late payments as applicable at the time when the credit agreement was concluded, and the arrangements for its adjustment and, where applicable, any charges payable for default, | ||

(m) a warning regarding the consequences of missing payments, | ||

(n) the sureties and insurance required, if any, | ||

(o) the existence or absence of a right of withdrawal, the period during which that right may be exercised and other conditions governing the exercise of that right, including information concerning the obligation of the consumer to pay the capital drawn down and the interest in accordance with Regulation 17(3)(b) and the amount of interest payable per day, | ||

(p) where applicable, information concerning the rights resulting from Regulation 18 and the conditions for the exercise of those rights, | ||

(q) the right of early repayment, the procedure for early repayment, and, where applicable, information about the creditor’s right to compensation and the way in which that compensation will be determined, | ||

(r) the procedure to be followed in exercising the right of termination of the credit agreement, | ||

(s) whether or not there is an out-of-court complaint and redress mechanism for the consumer and, if so, the methods for having access to it, | ||

(t) any other contractual terms and conditions, and | ||

(u) where applicable, the name and address of the competent supervisory authority. | ||

(4) Where paragraph (3)(i) applies to a credit agreement, the creditor concerned shall make available to the consumer concerned, free of charge and at any time throughout the duration of the credit agreement, a statement of account in the form of an amortisation table. | ||

(5) An amortisation table shall indicate the payments owing and the periods and conditions relating to the payment of such amounts. The table shall contain a breakdown of each repayment showing capital amortisation, the interest calculated on the basis of the borrowing rate and, where applicable, any additional costs. Where the interest rate is not fixed or the additional costs may be changed under the credit agreement, the amortisation table shall indicate, clearly and concisely, that the data contained in the table will remain valid only until the borrowing rate or the additional costs are changed in accordance with the credit agreement. | ||

(6) In the case of a credit agreement under which payments made by the consumer do not give rise to an immediate corresponding amortisation of the total amount of credit, but are used to constitute capital during periods and under conditions laid down in the credit agreement or in an ancillary agreement, the information required by paragraph (3) shall include a clear and concise statement that such credit agreements do not provide for a guarantee of repayment of the total amount of credit drawn down under the credit agreement, unless such a guarantee is given. | ||

(7) In the case of a credit agreement in the form of an overdraft facility where the credit has to be repaid on demand or within 3 months, the following shall be specified in a clear and concise manner: | ||

(a) the type of credit; | ||

(b) the identities and geographical addresses of the contracting parties as well as, if applicable, the identity and geographical address of the credit intermediary involved; | ||

(c) the duration of the credit agreement; | ||

(d) the total amount of the credit and the conditions governing the drawdown; | ||

(e) the following information in relation to borrowing rates and charges: | ||

(i) the borrowing rate; | ||

(ii) the conditions governing the application of the borrowing rate; | ||

(iii) where available, any index or reference rate applicable to the initial borrowing rate; | ||

(iv) the periods, conditions and procedure for changing the borrowing rate; | ||

(v) if different borrowing rates apply in different circumstances, the information referred to in sub-subparagraphs (i) to (iv) in respect of all the applicable rates; | ||

(f) an indication that the consumer may be requested to repay the amount of credit in full on demand at any time; | ||

(g) conditions governing the exercise of the right of withdrawal from the credit agreement; | ||

(h) information concerning the charges applicable from the time such agreements are concluded and, if applicable, the conditions under which those charges may be changed. | ||

(8) Nothing in this Regulation affects the operation of any law of the State regarding the conclusion of credit agreements if the law is not inconsistent with this Regulation. | ||

(9) A creditor or credit intermediary that contravenes a provision of this Regulation commits an offence. | ||

Information concerning changes in borrowing rates | ||

14. (1) Where applicable, subject to paragraph (2), a creditor shall inform a consumer of any change in the borrowing rate, on paper or another durable medium, before the change enters into force. The information shall state the amount of the payments to be made after the entry into force of the new borrowing rate and, if the number or frequency of the payments changes, particulars of the changes. | ||

(2) The parties may agree in the credit agreement that the information referred to in paragraph (1) is to be given to the consumer periodically where— | ||

(a) the change in the borrowing rate is caused by a change in a reference rate, | ||

(b) the new reference rate is made publicly available by appropriate means, and | ||

(c) information concerning the new reference rate is kept available on the premises of the creditor. | ||

(3) A creditor that contravenes a provision of this Regulation commits an offence. | ||

Obligations in relation to overdraft facilities | ||

15. (1) Where a credit agreement covers credit in the form of an overdraft facility, the creditor shall keep the consumer regularly informed by means of a statement of account, on paper or on another durable medium, containing the following particulars: | ||

(a) the precise period to which the statement of account relates; | ||

(b) the amounts and dates of drawdowns; | ||

(c) the balance from the previous statement, and the date of that balance; | ||

(d) the new balance; | ||

(e) the dates and amounts of payments made by the consumer; | ||

(f) the borrowing rate applied; | ||

(g) any charges that have been applied; | ||

(h) where applicable, the minimum amount to be paid. | ||

(2) Subject to paragraph (3), the consumer shall be informed on paper or another durable medium of any increase in the borrowing rate, or in any charge payable, before the change enters into force. | ||

(3) The parties may agree in the credit agreement that information concerning changes in the borrowing rate is to be given in the manner provided for in paragraph (1) where— | ||

(a) the change in the borrowing rate is caused by a change in a reference rate, | ||

(b) the new reference rate is made publicly available by appropriate means, and | ||

(c) information concerning the new reference rate is kept available on the premises of the creditor. | ||

(4) A creditor that contravenes a provision of this Regulation commits an offence. | ||

Termination of open-end credit agreements | ||

16. (1) A consumer may effect the standard termination of an open-end credit agreement free of charge at any time unless the parties have agreed on a period of notice. Such a period may not exceed one month. | ||

(2) If agreed in the relevant credit agreement, the creditor may effect the standard termination of an open-end credit agreement by giving the consumer at least 2 months’ notice on paper or on another durable medium. | ||

(3) If agreed in the credit agreement concerned, a creditor may, for objectively justified reasons, terminate a consumer’s right to draw down on an open-end credit agreement. The creditor shall inform the consumer of the termination and the reasons for it on paper or on another durable medium, where possible before the termination and at the latest immediately afterwards, unless the provision of that information is prohibited by another law or is contrary to objectives of public policy or public security. | ||

Right of withdrawal | ||

17. (1) A consumer may, within 14 calendar days after the relevant day specified in paragraph (2), withdraw from a credit agreement without giving any reason. | ||

(2) That period for withdrawal begins on— | ||

(a) the day on which the credit agreement was concluded, or | ||

(b) the day on which the consumer receives the contractual terms and conditions and information in accordance with Regulation 13, if that day is later than the date referred to in subparagraph (a). | ||

(3) If a consumer exercises the right of withdrawal— | ||

(a) to give effect to the withdrawal before the expiry of the deadline referred to in paragraph (1), he or she shall so notify the creditor in accordance with the information provided by the creditor pursuant to Regulation 13(3)(o) by a means that allows service of the notice to be proved in accordance with law, and | ||

(b) he or she shall pay to the creditor the capital and the interest accrued on it (at the agreed borrowing rate) from the date the credit was drawn down until the date the capital is repaid, without any undue delay and no later than 30 calendar days after the dispatch of the notification of the withdrawal. | ||

(4) The requirements of paragraph (3)(a) shall be taken to have been met if the notification— | ||

(a) is on paper or on another durable medium that is available and accessible to the creditor, and | ||

(b) is dispatched before the end of the period referred to in paragraph (1). | ||

(5) A creditor shall not be entitled to any other compensation from a consumer in the event of withdrawal, except compensation for any non-refundable charges paid by the creditor to a public administrative body. | ||

(6) If an ancillary service relating to a credit agreement is provided by the creditor concerned or by a third party on the basis of an agreement between the third party and the creditor, the consumer concerned is no longer bound by the ancillary service contract if the consumer exercises the right of withdrawal from the credit agreement in accordance with this Regulation. | ||

(7) If a consumer has a right of withdrawal under this Regulation, Regulations 10 and 11 of the Distance Marketing Regulations and Regulation 5 of the European Communities (Cancellation of Contracts Negotiated away from Business Premises) Regulations 1989 ( S.I. No. 224 of 1989 ) do not apply. | ||

(8) This Regulation is without prejudice to any other law establishing a period of time during which the performance of a contract may not begin. | ||

Linked credit agreements | ||

18. (1) Where a consumer has exercised a right of withdrawal from a credit agreement (being a right of withdrawal conferred by a law of the State giving effect to an Act of the European Communities or the European Union concerning a contract for the supply of goods or services), he or she also ceases to be bound by any linked credit agreement. | ||

(2) Where the goods or services covered by a linked credit agreement are not supplied, or are supplied only in part, or are not in conformity with the contract for their supply, the consumer has the right to pursue remedies against the creditor if the consumer has pursued remedies against the supplier but has failed to obtain the satisfaction to which he or she is entitled according to the law or the contract for the supply of the goods or services. | ||

Early repayment | ||

19. (1) A consumer may at any time discharge fully or partially his or her obligations under a credit agreement. In such cases, he or she is entitled to a reduction in the total cost of the credit to the extent of the interest and the costs for the remaining duration of the agreement. | ||

(2) Subject to paragraphs (3) to (6), in the event of early repayment of credit the creditor concerned is entitled to fair and objectively justified compensation for possible costs directly linked to the early repayment if the early repayment falls within a period for which the borrowing rate is fixed. | ||

(3) Such compensation may not exceed— | ||

(a) if the period between the early repayment and the agreed termination of the credit agreement exceeds one year, one per cent of the amount of credit repaid early, or | ||

(b) if that period is one year or less, 0.5 per cent of the amount of credit repaid early. | ||

(4) A creditor is not entitled to compensation— | ||

(a) if the repayment has been made under an insurance contract intended to provide a credit repayment guarantee, | ||

(b) in the case of an overdraft facility, or | ||

(c) if the repayment falls within a period for which the borrowing rate is not fixed. | ||

(5) A creditor is entitled to compensation under this Regulation only if the amount of early repayment exceeds €10,000 within any period of 12 months. | ||

(6) Any compensation shall not exceed the amount of interest the consumer would have paid during the period between the early repayment and the agreed date of termination of the credit agreement. | ||

Assignment of creditors’ rights | ||

20. (1) If a creditor’s rights under a credit agreement or the agreement itself are assigned to a third party, the consumer concerned is entitled to plead against the assignee any defence available to him or her against the original creditor, including set-off. | ||

(2) The consumer shall be informed of an assignment referred to in paragraph (1) except where the original creditor, by agreement with the assignee, continues to service the credit vis--vis the consumer. | ||

Overrunning | ||

21. (1) If a creditor and a consumer agree to open a current account, and there is a possibility of the consumer being allowed an overrun, the agreement shall contain the information referred to in Regulation 9(1)(e). The creditor shall provide that information on paper or on another durable medium on a regular basis. | ||

(2) If a significant overrunning continues for longer than one month, the creditor shall inform the consumer without delay, on paper or on another durable medium— | ||

(a) of the overrunning, | ||

(b) of the amount involved, | ||

(c) of the borrowing rate, and | ||

(d) of any penalties, charges or interest on arrears applicable. | ||

(3) This Regulation is without prejudice to any other law requiring a creditor to offer another kind of credit product when the duration of an overrunning is significant. | ||

(4) A creditor or credit intermediary that contravenes a provision of this Regulation commits an offence. | ||

PART 5 Annual percentage rate of charge | ||

Calculation of annual percentage rate of charge | ||

22. (1) The annual percentage rate of charge (equating, on an annual basis, to the present value of all commitments (drawdowns, repayments and charges), future or existing, agreed by the creditor and consumer concerned) shall be calculated in accordance with the mathematical formula set out in Part I of Schedule 1. | ||

(2) For the purpose of calculating the annual percentage rate of charge, the total cost of the credit to the consumer shall be determined, with the exception of— | ||

(a) any charges payable by the consumer for non-compliance with any commitments laid down in the credit agreement, and | ||

(b) charges (other than the purchase price) that, for purchases of goods or services, he or she is obliged to pay whether the transaction is effected in cash or on credit. | ||

(3) The costs of maintaining an account recording payment transactions and drawdowns, the costs of using a means of payment for payment transactions and drawdowns, and any other costs relating to payment transactions shall be included in the total cost of credit to the consumer unless— | ||

(a) the opening of such an account is optional, and | ||

(b) the costs of the account have been clearly and separately shown in the credit agreement or in another agreement concluded with the consumer. | ||

(4) The calculation of the annual percentage rate of charge shall be based on the assumptions that— | ||

(a) the credit agreement is to remain valid for the period agreed, and | ||

(b) the creditor and the consumer will fulfil their obligations under the terms of, and by the dates specified in, the credit agreement. | ||

(5) In the case of a credit agreement allowing variations in the borrowing rate and, where applicable, charges contained in the annual percentage rate of charge but unquantifiable at the time of calculation, the annual percentage rate of charge shall be calculated on the assumption that the borrowing rate and other charges will remain fixed in relation to the initial level and will remain applicable until the end of the credit agreement. | ||

(6) Where necessary, the additional assumptions set out in Schedule 1 may be used in calculating the annual percentage rate of charge. | ||

PART 6 Credit intermediaries | ||

Obligations of credit intermediaries | ||

23. (1) A credit intermediary shall indicate in advertising and documentation intended for consumers the extent of his or her powers, in particular whether he or she works exclusively with one or more creditors or as an independent broker. | ||

(2) A credit intermediary shall ensure that any fee payable by a consumer to the credit intermediary for his or her services is disclosed to the consumer, and agreed between the consumer and the credit intermediary on paper or on another durable medium before the relevant credit agreement is concluded. | ||

(3) A credit intermediary shall ensure that any fee payable by a consumer to the credit intermediary for the credit intermediary’s services is communicated to the creditor by the credit intermediary for the purpose of calculation of the annual percentage rate of charge. | ||

(4) A credit intermediary that contravenes a provision of this Regulation commits an offence. | ||

PART 7 Miscellaneous | ||

Anti-avoidance | ||

24. (1) A provision of a credit agreement that purports to disapply to the agreement any provision of these Regulations, or to alter in any respect the operation of any provision of these Regulations in relation to the agreement, is of no effect. | ||

(2) Without limiting the generality of paragraph (1)— | ||

(a) if a credit agreement has a close link with the State such that the law of the State would apply to it, but a provision of the agreement purports to apply the law of another country, the provision is of no effect, and | ||

(b) if— | ||

(i) an arrangement is in real terms a single transaction or a single commercial arrangement that would give rise to a credit agreement to which these Regulations would apply, but is cast in a form such that these Regulations apparently do not apply to it, and | ||

(ii) it appears that the agreement was cast in that form for the purpose of avoiding the application of these Regulations, | ||

a court shall have regard to the commercial reality of the transaction for the purpose of determining whether or not these Regulations apply to it. | ||

Penalties | ||

25. (1) A person who is guilty of an offence under these Regulations is liable— | ||

(a) on summary conviction, to a fine not exceeding €3,000 or imprisonment for a term not exceeding 12 months or both, or | ||

(b) on conviction on indictment, to a fine not exceeding €100,000 or imprisonment for a term not exceeding 3 years or both. | ||

(2) Where a person is convicted of an offence under these Regulations and there is a continuation of the offence by the person after his or her conviction, the person commits a further offence on every day on which the contravention continues and for each such offence is liable— | ||

(a) on summary conviction, to a fine not exceeding €1,000, or | ||

(b) on conviction on indictment, to a fine not exceeding €10,000. | ||

(3) Where an offence referred to in paragraph (1) or (2) is proved to have been committed by a body corporate with the consent, connivance or approval of, or to be attributable to the wilful neglect of, a person— | ||

(a) who is a director, manager, secretary or other officer of the body corporate, or | ||

(b) who purported to act in any such capacity, | ||

that person as well as the body corporate commits an offence and is liable to be proceeded against and punished as if he or she were guilty of the first-mentioned offence. | ||

(4) A person may be charged with an offence under paragraph (3) even if the body corporate concerned is not charged with any offence under these Regulations in relation to the same matter. | ||

(5) Summary proceedings in relation to an offence under these Regulations may be prosecuted by the Central Bank and Financial Services Authority of Ireland. | ||

Regulation of certain friendly societies for certain purposes. | ||

26. The Irish Financial Services Regulatory Authority is the regulator of friendly societies, other than any to which Parts 2 to 6 and this Part do not apply, in relation to compliance with Parts 2 to 6 and this Part. | ||

PART 8 Amendments of other statutory instruments | ||

Amendment of Distance Marketing Regulations | ||

27. (1) The European Communities (Distance Marketing of Consumer Financial Services) Regulations 2004 ( S.I. No. 853 of 2004 ) are amended in Schedule 2 by inserting after subparagraph (b) the following: | ||

“(ba) where the financial service is a credit agreement to which the European Communities (Consumer Credit Agreements) Regulations 2010 (S.I. No. of 2010) apply, the following particulars: | ||

(i) the total amount of credit and the conditions governing its drawdown; | ||

(ii) the duration of the credit agreement; | ||

(iii) in the cases of credit in the form of deferred payment for a specific good or service and a linked credit agreement, the good or service concerned and its cash price; | ||

(iv) the following information in relation to borrowing rates and charges: | ||

(I) the initial borrowing rate; | ||

(II) the conditions governing the application of the initial borrowing rate; | ||

(III) where available, any index or reference rate applicable to the initial borrowing rate; | ||

(IV) the periods, conditions and procedure for changing the borrowing rate; | ||

(V) if different borrowing rates apply in different circumstances, the information required by sub-subparagraphs (i) to (iv) for all the applicable rates; | ||

(v) the amount, number and frequency of payments to be made by the consumer and, where applicable, the order in which payments will be allocated to different outstanding balances charged at different borrowing rates for the purposes of reimbursement; | ||

(vi) the annual percentage rate of charge illustrated by means of a representative example;”. | ||

SCHEDULE 1 Methods of calculating annual percentage rate of charge | ||

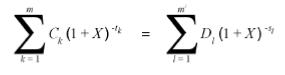

PART 1 Basic equation expressing equivalence of drawdowns with repayments and charges | ||

The basic equation, which establishes the annual percentage rate of charge (APR), equates, on an annual basis, the total present value of drawdowns on the one hand and the total present value of repayments and payments of charges on the other hand, i.e.: | ||

| ||

| ||

where: | ||

X is the APR, | ||

m is the number of the last drawdown, | ||

k is the number of a drawdown, thus 1 k m, | ||

Ck is the amount of drawdown k, | ||

tk is the interval, expressed in years and fractions of a year, between the date of the first drawdown and the date of each subsequent drawdown, thus t1 = 0, | ||

m / is the number of the last repayment or payment of charges, | ||

l is the number of a repayment or payment of charges, | ||

Dl is the amount of a repayment or payment of charges, | ||

sl is the interval, expressed in years and fractions of a year, between the date of the first drawdown and the date of each repayment or payment of charges. | ||

Remarks: | ||

(a) The amounts paid by both parties at different times shall not necessarily be equal and shall not necessarily be paid at equal intervals. | ||

(b) The starting date shall be that of the first drawdown. | ||

(c) Intervals between dates used in the calculations shall be expressed in years or in fractions of a year. A year is presumed to have 365 days (or 366 days for leap years), 52 weeks or 12 equal months. An equal month is presumed to have 30.41666 days (i.e. 365/12) regardless of whether or not it is a leap year. | ||

(d) The result of the calculation shall be expressed with an accuracy of at least one decimal place. If the figure at the following decimal place is greater than or equal to 5, the figure at that particular decimal place shall be increased by one. | ||

(e) The equation can be rewritten using a single sum and the concept of flows (Ak), which will be positive or negative, in other words either paid or received during periods 1 to k, expressed in years, i.e.: | ||

| ||

| ||

S being the present balance of flows. If the aim is to maintain the equivalence of flows, the value will be zero. | ||

PART 2 Additional assumptions for calculation of annual percentage rate of charge | ||

(a) if a credit agreement gives the consumer freedom of drawdown, the total amount of credit shall be deemed to be drawn down immediately and in full; | ||

(b) if a credit agreement provides different ways of drawdown with different charges or borrowing rates, the total amount of credit shall be deemed to be drawn down at the highest charge and borrowing rate applied to the most common drawdown mechanism for this type of credit agreement; | ||

(c) if a credit agreement gives the consumer freedom of drawdown in general but imposes, amongst the different ways of drawdown, a limitation with regard to the amount and period of time, the amount of credit shall be deemed to be drawn down on the earliest date provided for in the agreement and in accordance with those drawdown limits; | ||

(d) if there is no fixed timetable for repayment, it shall be assumed: | ||

(i) that the credit is provided for a period of one year; and | ||

(ii) that the credit will be repaid in 12 equal instalments and at monthly intervals; | ||

(e) if there is a fixed timetable for repayment but the amount of such repayments is flexible, the amount of each repayment shall be deemed to be the lowest for which the agreement provides; | ||

(f) unless otherwise specified, where the credit agreement provides for more than one repayment date, the credit is to be made available and the repayments made on the earliest date provided for in the agreement; | ||

(g) if the ceiling applicable to the credit has not yet been agreed, that ceiling is assumed to be €1,500; | ||

(h) in the case of an overdraft facility the total amount of credit shall be deemed to be drawn down in full and for the whole duration of the credit agreement. If the duration of the credit agreement is not known the annual percentage rate of charge shall be calculated on the assumption that the duration of the credit is three months; | ||

(i) if different interest rates and charges are offered for a limited period or amount, the interest rate and the charges shall be deemed to be the highest rate for the whole duration of the credit agreement; | ||

(j) for consumer credit agreements for which a fixed borrowing rate is agreed in relation to the initial period, at the end of which a new borrowing rate is determined and subsequently periodically adjusted according to an agreed indicator, the calculation of the annual percentage rate shall be based on the assumption that, at the end of the fixed borrowing rate period, the borrowing rate is the same as at the time of calculating the annual percentage rate, based on the value of the agreed indicator at that time. | ||

SCHEDULE 2 Standard European Consumer Credit Information Form | ||

1. Name and contact details of the creditor and any credit intermediary | ||

| ||

Wherever “if applicable” is indicated, the creditor must fill in the box if the information is relevant to the credit product or delete the respective information or the entire row if the information is not relevant for the type of credit considered. | ||

Indications between square brackets provide explanations for the creditor and must be replaced with the corresponding information. | ||

2. Description of the main features of the credit product | ||

| ||

3. Costs of the credit | ||

| ||

4. Other important legal aspects | ||

| ||

If applicable | ||

5. Additional information in the case of distance marketing of financial services | ||

| ||

[*] This information is optional for the creditor. | ||

SCHEDULE 3 European Consumer Credit Information Form for overdrafts, consumer credit offered by certain credit organisations and debt conversion | ||

1. Name and contact details of the creditor and any credit intermediary | ||

| ||

Wherever “if applicable” is indicated, the creditor must fill in the box if the information is relevant to the credit product or delete the respective information or the entire row if the information is not relevant for the type of credit considered. | ||

Indications between square brackets provide explanations for the creditor and must be replaced with the corresponding information. | ||

[*] This information is optional for the creditor. | ||

2. Description of the main features of the credit product | ||

| ||

3. Costs of the credit | ||

| ||

4. Other important legal aspects | ||

| ||

If applicable | ||

5. Additional information to be given where the pre-contractual information is provided by a credit union or relates to a consumer credit for debt conversion | ||

| ||

If applicable | ||

6. Additional information to be given in the case of distance marketing of financial services | ||

| ||

[*] This information is optional for the creditor. | ||

| ||

GIVEN under my Official Seal, | ||

9 June 2010. | ||

BRIAN LENIHAN, | ||

Minister for Finance. | ||

EXPLANATORY NOTE | ||

(This note is not part of the Instrument and does not purport to be a legal interpretation.) | ||

These regulations transpose into domestic law the provisions of the Consumer Credit Directive 2008/48/EC of the European Parliament and of the Council on credit agreements for consumers. That Directive establishes a harmonised legal framework in the European Union for the provision of consumer credit ranging from €200 to €75,000. It does not apply to mortgages. It replaced a 1987 Directive (87/102/EEC), which laid down minimum rules for consumer credit agreements within the EU and which was transposed into domestic law by the Consumer Credit Act 1995 . | ||

The Regulations have the following benefits for consumers: | ||

•Standardisation of pre-contractual information through the use of the Standard European Consumer Credit Information form (SECCI) and standardisation of the information to be contained in a credit agreement. | ||

•The Annual Percentage Rate of charge (APR) will be more transparent and will include all known costs and assumptions used in calculation. This will provide an effective tool for comparisons between loans offered by creditors. | ||

•Consumer Protection will be enhanced through more adequate explanations, creditworthiness checks and credit history checks. | ||

•In the case of credit intermediaries, all fees and ties with the credit provider must be provided for in the advertising and in the documentation provided to the consumer. The fees for the credit intermediary must also be included in the APR quoted to the consumer. | ||

•The Directive provides that compensation for early repayment of fixed rate loans may not exceed 1% (or 0.5% if less than a year remains on the fixed rate) of the amount of the credit repaid early. The creation of a threshold of €10,000 under which early repayment fees will not be charged in any one year provides enhanced benefits to consumers to repay early when the opportunity arises. | ||

•Full 14 day “Right of Withdrawal” applies to all credit agreements subject to the full provisions of the Directive. Option to waive the “Right of Withdrawal” is not permitted. | ||

1 OJ No. L133, 22.5.2008, p.66. | ||